Bubble Collapsing or Higher Upside Leg Coming?

Art is the lie that reveals the truth - Pablo Picasso

I want to invite you to a mental experiment based on a prior very challenging, global macro environment that could help in making resilient decisions for the highly volatile global macro environment of today. It also supports why I think there is still a higher upside leg coming in tech stocks.

Let’s examine the thinking process of Franz, a hypothetical trader, investing in Japanese equities in 1985 when many events challenged viewpoints and positions.

Japan Equity Index. From 1985 to 1995.

When Franz began his work, the Japanese Yen was extremely devalued with respect to the USD, making Japanese products cheaper and more competitive. Ronald Reagan had been placing stringent tariffs against motorcycles and cars. In 1985, the Plaza Accord was a joint-agreement signed between France, West Germany, Japan, and the United States to engineer the devaluation of the US Dollar in relation to the Japanese Yen and German Deutsche Mark. With the planned appreciation of the Japanese Yen, Franz eagerly jumped into the Japanese equity market, having a sort of government insurance backing his portfolio.

It started off very profitable. Beginning in January of 1985, with the Nikkei at 12,000, the index soared to 16,870 by April of the following year. It was a massive bull market run. Some analysts along the way were pointing out that the market was overvalued, and the Japanese equity market was a bubble. However, there were so many investors not familiar with investing in Japan, that Franz remained very bullish on the Nikkei.

Chernobyl

Then, one morning in April of 1986, the news captured his attention. The Soviets were having big problems in Chernobyl with their nuclear facility. The ongoing Cold War was a game of mutual assurance. The US could not use nuclear weapons against the Soviets and vice-versa. because it would imply mutual annihilation. This catastrophic disaster completely changed the geopolitical balance.

Franz thought about what the implications would be for the stock market. How will it affect my existing positions in the Nikkei? Will there be any interesting trade opportunities?

Geopolitically, this immediately appears to be a tremendous opportunity for Reagan and the United States. The odds of winning the Cold War would be easily tipped in their favor. This is great news for my portfolio. Japan still has a strong competitive advantage. They can sell semiconductors produced in Japan to the US, but American semiconductor manufacturers cannot sell to Japan.

The rise of the Japanese market would continue. The news of success of the Japanese companies will attract more and more inflows, while more and more trade barriers from the Reagan administration confirmed that Japanese companies enjoyed a very strong competitive advantage. A strong Yen would undermine the Japanese economic growth however, as the government still had the fiscal and monetary option.

By June 1987, Franz had made a killing, the Nikkei had more than doubled to 25,036. The Japanese Yen was too strong however, as economic growth was dependent on exports and turned sluggish.

USDJPY appreciation between 1985 and 1992. Source: Tradingview.

As the Franz thinking process was described, the Japanese government was now playing the fiscal and monetary card to curb the impact of a strong Yen in the Japanese economy. Franz was nervous as everybody was talking about a bubble in Japanese equities, but still, he remained bullish. He felt that the move in the Yen was too quick and too large. There was still liquidity and companies were still heavily investing in plants and equipment, he thought. Reagan was all in against the Soviets.

Franz stayed long.

The 1987 Crash

The market continued running up, monetary easing and fiscal spending was successful in feeding the animal spirits and the Nikkei surpassed new highs. As shorting activity increased, the conundrum of analysts and traders continued to predict an imminent bubble crash in Japan…

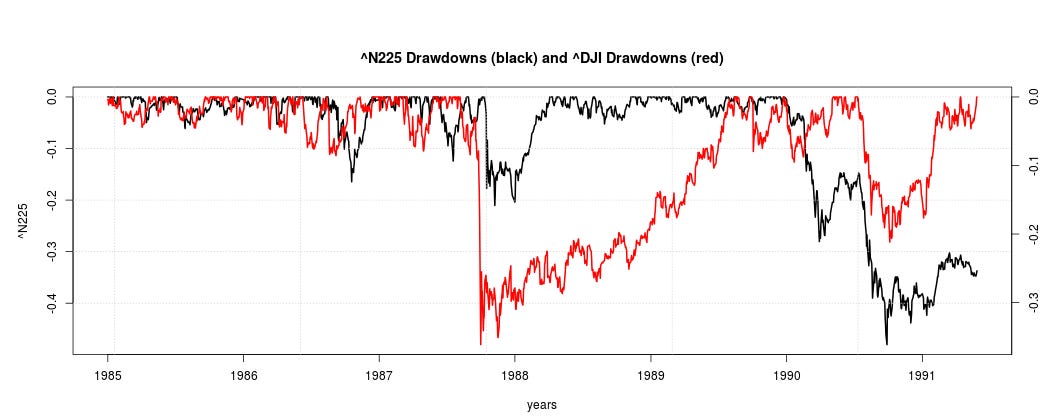

Then, on Monday, October 19, the Dow Jones crashed 22% in one day. Equities across the US were in free fall. Franz ran to close all of his positions; if the Dow crashed like this, then surely Japan would tank as well. At the time it was not clear why the markets were crashing, and it is still not clear today.

Japan lost only 15% compared to 22% in the US and an astounding 40% in Hong Kong. Some argued that one of the reasons for the crash was the Plaza Accord. The propped up, strong Japanese Yen was greatly affecting Japanese investor’s foreign investments, repatriation of capital and impulse buying of Japanese equities. It also created liquidity problems in the US, and while the crash was not fully explained by this factor, it was part of the context necessary for the crash to happen. It allowed panic to cascade, from hedges, to margin calls and ultimately a fat tail event: the Black October Crash.

Franz remained tight in his position and worried about potential ripple effects of the US crash. He was surprised by the speedy recovery in Japan. Government fiscal spending and monetary stimulus was working to restore the equity markets. Franz knew that was the last game in the town and he built a long position again in April 1988.

The market was moving in his direction.

The Fall of the Berlin Wall

In November of 1989, the Nikkei was 30% up from the levels where Franz began his new long position. However, the times never ceased to surprise him. The Berlin Wall was brought down… Reagan had won.

Franz recognized that a new world was emerging. Japan would no longer be the winner in this new configuration. He had amassed a small fortune trading Japanese equities and now it was time for him to make a change in his life. He proposed to his girlfriend Agnieszka, and they would move to Thailand. His friend John had told him it was a paradise and perhaps an interesting investment opportunity.

Lessons:

We are living in a very important tipping point and our allocation must be resilient to high increases of volatility. There are trade ideas that are agile in the current global macro environment, but technology equity is still one of these ideas… the rewiring of globalization is the big thing here.

Technology ETF XLK

Part of this phenomenon was oil prices in the first half of 2020. Factories coming back to Japan, US and Europe are still not priced in. Flows back to the US could create an accident in highly leveraged emerging markets. Hong Kong seems not to be as relevant as Shanghai for the communist party in China. This implies an important change in the structure of capital flows in Asia. Furthermore, Korean conglomerates (Chaebols) were one player that benefited from the global carry trade. The thirst for corporate debt has been the lifeblood of survival for many zombie companies with an unprofitable business model for years.

A potential cold war of sorts between China and the US could lead to a reshuffling of capital flows across the Asia Pacific.

Drawdowns in technology ETF (XLK) vs. Drawdowns Hong Kong ETF (EWH)

Europe also looks compromised geopolitically. Can France and Germany deal with Russian pressure in the Baltic, Belarus and Turkey in the Mediterranean?

The tech equity rally resembles the Japanese equity rally. In 1988, everybody hated the rally but it continued until a real game changer occurred. I think this game changer could be antitrust and taxes to big tech that would heavily affect companies like Facebook, Google, Apple, Amazon and even Netflix. However, there are many technology plays not related with the FAANGs that will be essential to expanding the growth of 5G telecommunications and a new manufacturing industrial revolution.

The world of bits needs electricity

As we stated in our April post, the world of bits is roaring while the world of things is in big trouble. If you feel uncomfortable investing in a market with such high valuations there are other ways to have exposure to the most important commodity in the world of bits: electricity.

One of our favorite plays is uranium. It is contrary to the current market architecture for oil, where the market is dominated by oversupply and an ongoing shift from the US as the main importer towards China persists. Electricity is fundamental for the development of a new manufacturing revolution, including AI empowered systems, electric cars, and smart cities. Uranium is the source for clean nuclear energy and despite it being demonized since Fukushima, it is actually very safe.

We expect demand for uranium will increase while the supply is very tight. One of the ways to play that is by investing in CAMECO (CCJ), one of the most important uranium producers in the world.

If you want to have access to our portfolio, in which our main objective is to outperform the S&P 500, through the use of trade ideas with high gain to pain ratios, please subscribe to our premium version either using a credit card in the substack platform or by sending 0.04 BTC yearly to our wallet.

38EM9eNSNxDYbkkfVnXLVM7j8goQdzzhDx

Guillermo Valencia

Co-founder Macrowise

September 7, 2020

Florinópolis, Brazil.