Conversation #1

Conversation #1

James Leitner and Guillermo Valencia on Global Macro, FX, Emerging Markets, SPX500 and Investment Tools.

The constantly changing world in which we live waits for no one. The cool, hip trend or way of doing business yesterday can change in a moment’s notice. It seems that nothing is set in stone. As the world evolves and new businesses and infrastructures take shape, it is only natural that the investment management process changes as well. Here at Macrowise, we are not only focused on keeping up with the trends, but identifying them and proactively searching for signals that will help investors better prepare for the landscape that lies ahead. More than just searching for good investment opportunities, we aim to create tools to empower investors and decision makers alike.

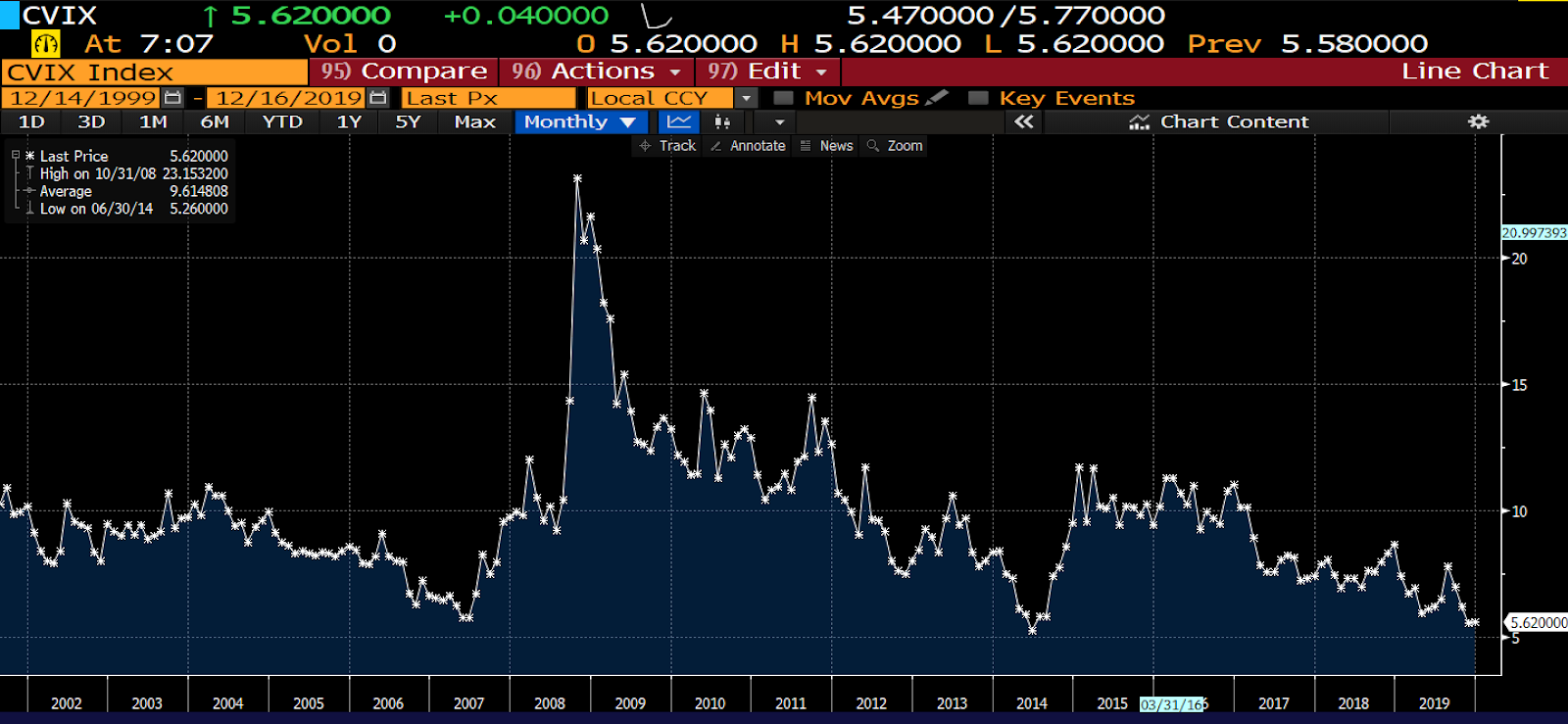

FX Volatility

Since 2013, the volatility in the FX market has declined precipitously and is now close to historic lows.However idiosyncratic volatility spikes have been experienced across a variety of currencies.

Source: Bloomberg.

Compare that to the volatility chart for the TRY going back over 10 years:

Source: Bloomberg.

The spike in the summer and fall of 2018 stands out with 3 month volatilities both implied and realized reaching almost 50 percent. The crash of the TRY combined with self referential feedback effects, stop losses and the subsequent rise of interest rates to levels of 23 percent and higher for long dated tenors, allowed for structures with phenomenal risk reward ratios to be established.

The lesson would appear to be that given the approximately 45 currency pairs which we monitor time will bring opportunities. As Jesse Livermore is reputed to have said ‘The hardest part is sitting on your hands”.

One question to be asked is whether in the nonlinear framework of currency volatilities the current low level allows for longer dated positions to be established looking at valuation mean reversion potential which would give directional guidance.

In this report, we will utilize the nonlinear framework of renowned physicist, Richard Feynman, that he applied toward better understanding the cause of the Challenger catastrophe and draw parallels to the happenings in the FX markets. We will also cover an interview with James Leitner, president of Falcon Management and Macrowise Co-Founder.

The Global Macro Manager

Steven Drobny’s book, Inside the House of Money describes James as one of the greatest macro traders that you’ve never heard of. He was once a currency expert on Wall Street, but now plays the game through his own family office. Much of his expertise can be attributed to his understanding of two of the most important governance system in our civilization: Markets and Democracy.

When we first met, I remember James talking about the need for curation tools from media to investment. We decided to join forces, combining our collective knowledge and ideas to create Macrowise. Our vision is to harness the power of algorithms to create better signals and construct creative frameworks designed to improve the investment decision making process. In a sea of noise it becomes more and more important to have methodologies to find the signal.

The Very Long Cycle

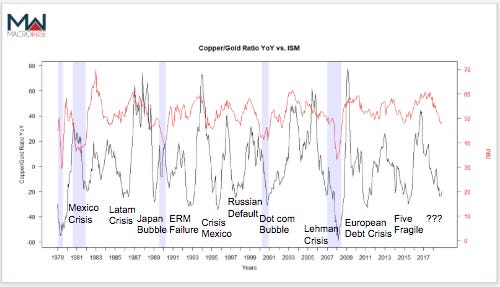

As recently as this year, many were predicting a recession due to the inversion of the treasuries curve, PMI levels below 50, and even the ratio between copper and gold. These signals seem to strongly indicate deceleration in the business cycle, but it is important to remember that deceleration does not always imply a recession.

ISM Vs Copper/Gold YoY. Source: Bloomberg.

When we created a set of signals to track the business cycle, the YoY copper to gold ratio revealed a lot of information. Since 1979, 13 decelerations to the global economy coincided with the ratio falling by about -15% or more, but only 5 resulted in a recession. However, all decelerations triggered idiosyncratic moves, half of which were directly linked to one or many emerging market countries, while the other half originated in developed markets but found echoes in emerging economies. The trade and capital flow linkages tied the network together in such a way that a disturbance anywhere could reverberate across the whole system. All of these cases also presented important opportunities to consider tipping points.

Tipping Points

Guillermo Valencia: Jim how can we trade these tipping points? How we can curate the information to avoid countries in crisis and get in early on the next big investment opportunity?

James Leitner: Let us first talk about curating. I am a big believer in finding ways to uncover systematically potential signals for use in investing. You need to ask yourself continuously what types of investment factors have worked historically and keep analyzing the world for setups that, using history as a guide, might be interesting. For example, we know that high yielding currencies on average outperform low yielding currencies. Well the least you can do is look at a forced ranking of currencies by yield to get a sense where you might find opportunity. Below you see the spread of rates with TRY at 10.5 percent ( down 55% from the high) and the HUF at the bottom with rates close to zero. Does it necessarily mean that TRYHUF is a good trade? Of course not. But one needs to keep looking for the signal systematically across as wide a range of asset classes as possible and methodologies as possible.

Source: Bloomberg.

One thing that i have noticed is a change in the importance of factors we follow. With most emerging markets now economically less stressed by traditional financial metrics the role of social and political indicators has grown in importance. So as we look across countries today we see that popular discontent as shown in demonstrations, violence on the street, public unrest, is seen across the world from Hongkong to Santiago. The underlying causes are all local and distinct and tipping points have become more idiosyncratic, driven by country specifics.

However there are some underlying drivers of economic insecurity and increased inequality which appear to link many of these public protest movements. The nonlinearity of the responses becomes evident when you see how for example Chile went from a poster child of economic success to a crucible of instability virtually within a week this fall. Change driven by politics has become more important to understand and analyse.

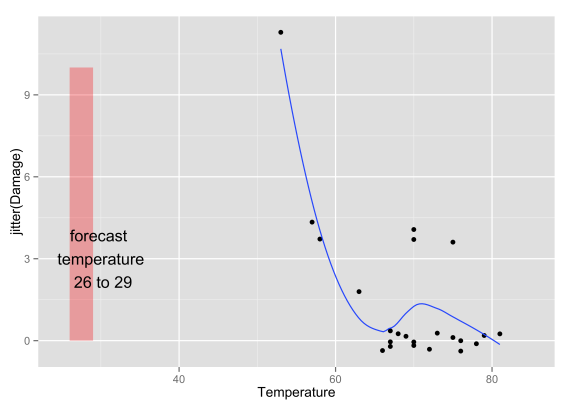

One of the best examples to understand a nonlinear system is given by Richard Feynman in regards to the explosion of the Challenger. After the space shuttle and its crew were destroyed in a catastrophic explosion on January 28, 1986, NASA appointed members of the Rogers Commission to investigate the cause of the disaster. When asked to be a part of this commission, Feynman was reluctant at first, but then accepted.

In order to find out what happened, Feynman went straight to the people who built the shuttle. This led him to not only realize what a risky business launching the shuttle really was, but ultimately was the key in discovering the cause of the explosion. NASA officials said that the chance of failure of the shuttle was about 1 in 100,000; Feynman found that number to be closer to 1 in 100. He uncovered that the rubber O-rings used to seal the rocket booster joints failed to expand when the temperature was at or below 32 degrees F (0 degrees C). This could be considered a phase change, a temperature which changed the basic behavior of the O-ring material. The temperature at the time of the Challenger liftoff was precisely that, 32 degrees F. Essentially there was a non linear tipping point at which O-rings changed in behavior such that they could not fulfill their original function as designed by the engineering process.

O-ring Failures vs Temperature. Source: NASA.

Merging the Macro with the Micro

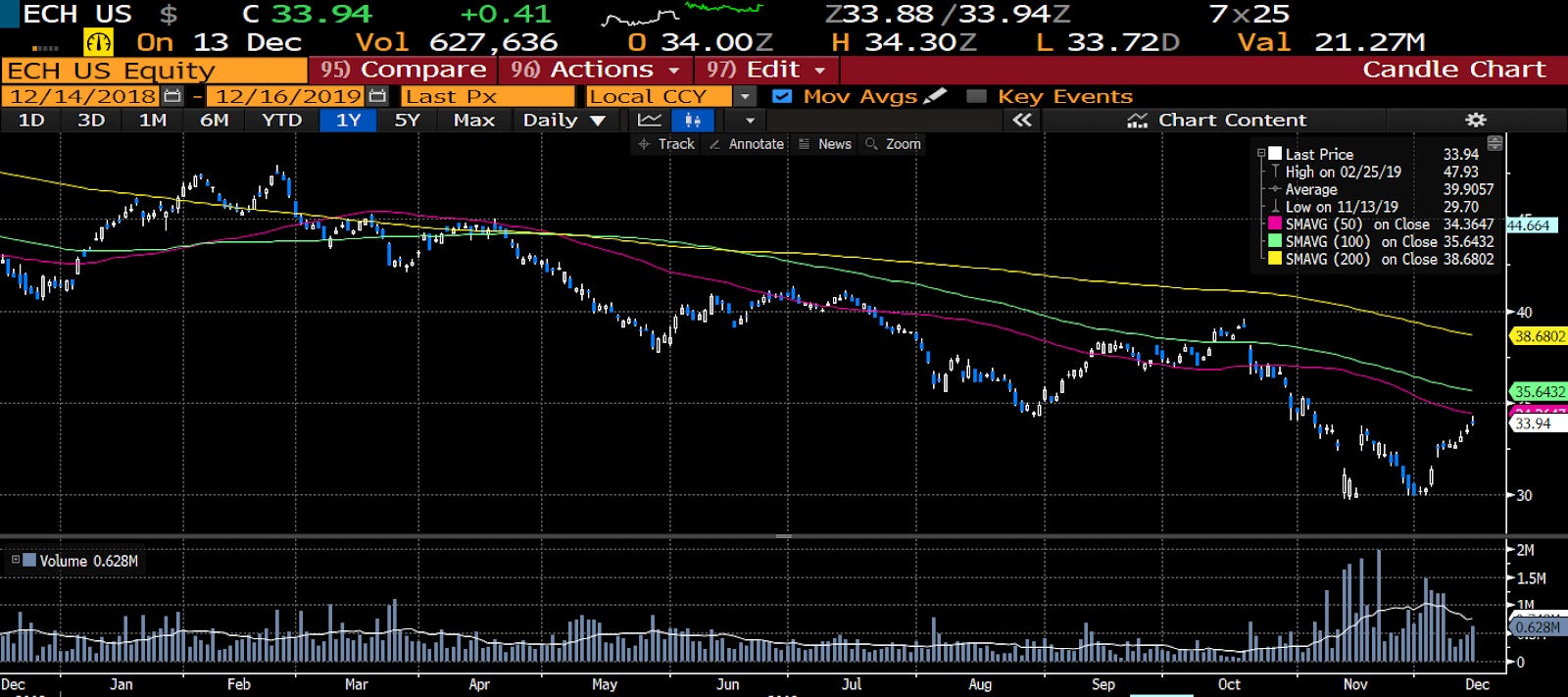

G.V: So, could there be a similar type of forecast that could be used as a barometer for a bear market in commodity dependent countries. The demonstrations in the streets of Chile and Colombia, as well as the millions of Venezuelans fleeing in an attempt to escape from oppression and misery among other points of tension dominate the region. Is it simply the fallout from the commodities cycle or is something bigger happening in regards to globalization?

J.L: I think that we need to become much more cognizant of social indicators in the countries where we are investing. It is not enough to merely look at company specific data on a micro level. There are plenty of companies that score well on all kinds of metrics whether financial or ESG in Chile, but it did not help them when the entire market cratered 25.5 percent over 4 weeks from October 18th to November 14th.

Source: Bloomberg

What I am calling for is a merging of the macro with the micro in the world of investing.

We should also be careful of the hype which tends to correlate with new acronyms. Take the emergence of the term BRICS and then compare that to the actual performance of the BRIC currencies. It is easy to get caught up in the narrative. Narrative matters tremendously but our thinking must be tempered with other inputs as well.

BRICS currencies 2011-2019. Source: Tradingview.

History, Outliers, China and Korea.

G.V: China’s continued determination to challenge the US for global influence dominates the current geopolitical arena. The rise of China is seen by many as an unavoidable event and remains on a collision course with the US. This situation, coined Thucydide’s trap by Graham T. Allison, where an established power is threatened by a growing rival often culminates in war. In order to avoid an all out war, the incumbent power and challenger must bargain with each other to diffuse this situation. The trade war is just the tip of the iceberg and the battle for world control and potential redefining of the new world order lie ahead.

Empires in 1300. Source: http://worldhistorymaps.info/maps.html

Before delving more into the current state of affairs, it’s important to remember that history can sometimes prove useful in helping to better understand the unexpected changes regarding geopolitics that could occur. So, let’s begin with the last real period when an Asian civilization was the dominant ruler, around 1300, when the Mongols ruled over one of the greatest empires the world has ever seen. The world economy was concentrated and flowed through Asia. The Mediterranean was an Islamic Lake and the geographical setting forced the non-relevant countries of the time (Portugal and Spain among others) to look for different avenues to grow and prosper as travel throughout the Mediterranean and into Asia was difficult. In the effort to find alternative trade routes and partners, the unexpected results included the coast of Africa and eventual discovery of America.

Source: Statista.

So, jump to the 21st century where the ocean is the Internet and the fight can essentially be split into two paradigms - one led by Silicon Valley in the US and the other of the challenger in China. The fortress walls are not made of bricks, but bits instead. Caught in the midst of this political tension between Western Powers and China is the Korean Peninsula. While South Korea is not the biggest protagonist in the world of software, it is a major player in the world of hardware. South Korea has the highest density of robots per human workers. The geopolitical spectrum seems very different in today’s world, but the tension between South Korea and Japan could alienate South Korea’s interest with China and lead them to more aggressively attempt to conquer the Internet out of necessity. Add to that North Korea’s potential to offer for cheap labor and propensity to conduct cyber warfare, the unification of the Koreas could be a game changer that few are expecting.

What are your thoughts on Southeast Asia and in particular South Korea?

J.L: I love the way you think outside the box. There is plenty of narrative about Korea to be found in the sell side literature we are inundated by and occasionally there is a reference to the possibility of unification but no one I know takes it into account in their investment decision making. What kind of optionality would we be looking for? FX, equity, other?

FX volatility is cheap again, but not yet at ridiculously cheap as it was in 2007 when I was able to buy 1 year dollar calls at sub 4 percent vol.

Source: Bloomberg.

Same with KOSPI volatility which is cheap versus historicals but not at the absolutely cheapest level ever.

Source:Bloomberg.

In the US I have been buying 1 year SPX call options which we can discuss later and I should be looking at ideas in Korea.

Poland

G.V: Some argue that the entire growth story concentrated in Asia and Europe is crumbling. However, this perception could be greatly underestimating one of the most amazing growth stories in emerging markets: Poland.

When comparing the development of Poland to Latin American countries, it is quite astonishing. Let’s do a quick comparison with Chile, once the most successful country in South America. Despite huge advances in economic development, little diversification of exports has come to fruition, as they remain heavily concentrated in raw materials. Poland is very different. They export a much more diversified array of products and the $212 billion worth of exports in 2018 was three times that of Chile. The other very important factor is that Poland is also home to a vast amount of shale gas reserves so it is one of the few countries that has hope for future energy independence in Europe.

Chile Exports 2018. Source: Observatory of Economic Complexity MIT.

Poland Exports 2018. Source: Observatory of Economic Complexity MIT.

Will Poland be able to evolve from a predominantly German factory into an important trade partner for others in Eurasia?

J.L: I think you make a good point with reference to Poland’s exports but here again i think you need to not overlook politics. The ‘rule of law’ in Poland is clearly challenged and over time that reflects itself in diminished equity market performance. The high point for the rule of law index happened in 2011 and it has consistently dropped since then. It is a worrying sign and both FDI and portfolio flows ought to be aware of growing risks. Although the currency is cheap based on behavioral and fundamental factors I am not involved in Poland.

US Elections and the SPX 500

G.V: Like marketplaces, politics seem to be an infinite game, where players and strategies can change at a moment’s notice. The objectives are perpetually in a state of change as well and the only certainty is that the game will continue. However, some players definitely do not understand this, or choose not to view it this way. We have elections coming up in the US, and Donald Trump appears to be playing a finite game. His values don’t exemplify a long-term strategy, as he seems to be focused on the short-term goal to win now.

Will Bloomberg or Warren be able to unite the American people in a quest to return it to the nation that the founding fathers intended? What do you think are the possible implications for the SPX 500 and markets as a whole?

J.L: I can only hope that the next president has a better understanding of history and what made the USA a superpower. Denigrating our allies, undermining the rule of law both internationally and domestically, increasing social and economic inequality, and very importantly pretending to believe that climate change is not an existential threat to humanity are all recipes for the US to underperform politically versus expectations. This does not mean that at this point the equity market needs to underperform. We have seen that the US market has outperformed on almost every possible metric other developed and emerging markets for the last ten years.

I would argue that this happened because austerity was not embedded in our system as it is in Europe and although modern monetary theory is being attacked using straw man arguments, at this point increased deficits here and in Japan have not led to the feared inflationary impulse many economists called for. Au contraire, we have by far outperformed economically, and whoever becomes president will continue with this policy, whether labelling it MMT or just sweeping deficits under the rug, as the republican party has done consistently.

The unaddressed problem by the republicans has been that the economic benefits of this policy have predominantly gone to the top 10 percent of earners, thus hollowing out society further.

It can only be hoped that a democratic administration will pursue ways to regrow the middle class, while focusing on the long run effects of better education and research to grow productivity.

As I look at the 2020 electoral cycle I see many more business friendly possibilities lining up with a tremendous amount of negativity and cash on the sidelines or under-investment in the equity markets. My favorite trade, which I implemented when the SPX broke 3000, was to buy 3500 to 4000 strike SPX call digital options for maturity in December 2020. The prices implied at that time a 1 in 6.6 chance that we would settle above 3500 and a 1 in 50 chance that we would settle above 4000. I believe those probabilities are way too low given the underlying outlook for no recession in 2020.

Amazon & Microsoft

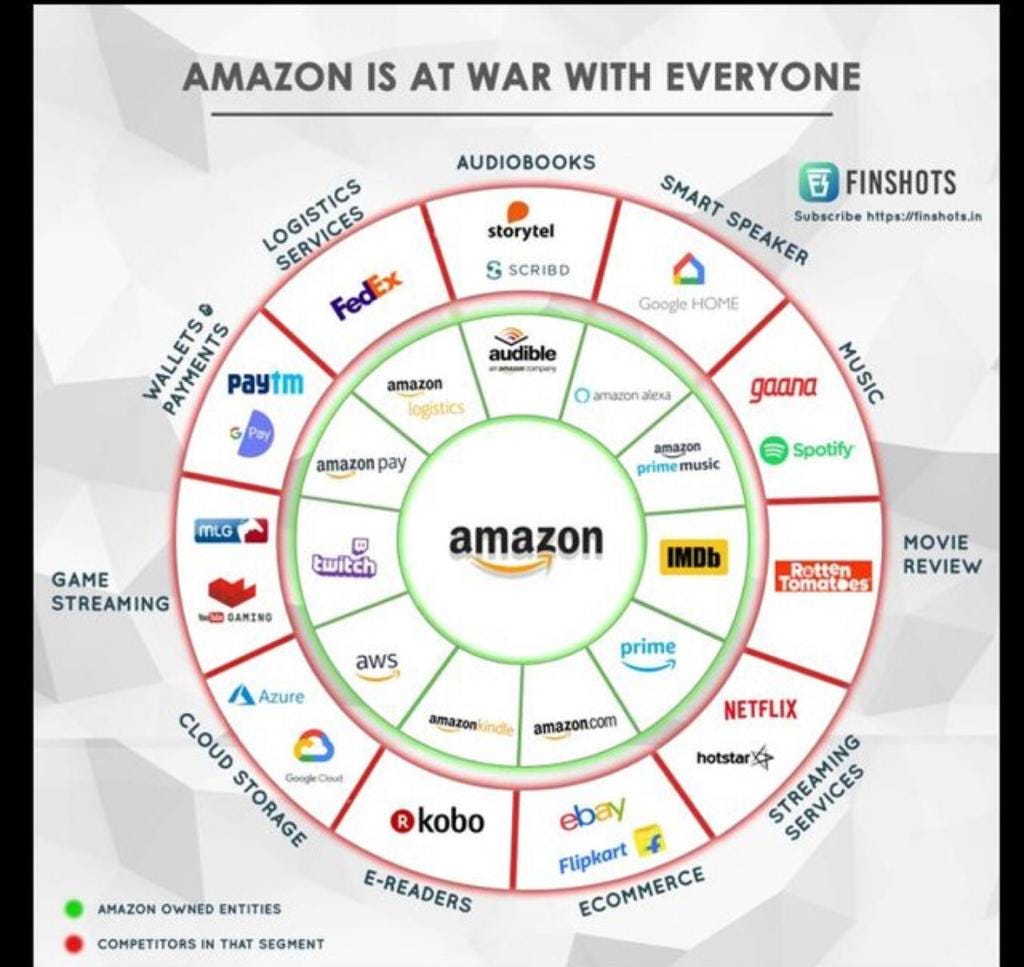

G.V: I love this trade! Let’s talk in more detail about US tech companies and the ETF heavyweights.My last question is about Amazon and Microsoft, both wonderful companies, but playing very different strategies. In some aspects, Amazon reminds me of the Soviet Union during the 80s, in the sense that they are involved in multiple battles on many fronts at the same time. Meanwhile, Microsoft’s vision seems more focused on their area of expertise as they continue empowering various software driven companies.

Source: Finshots.

Would it be fair for us to say that MSFT is playing with an infinite mindset, whereas AMZN is using a finite mindset strategy in your opinion? Long MSFT and short AMZN?

J.L: I so appreciate that you taught me about the finite and the infinite game view of life and thoroughly enjoyed the books you recommended (The Infinite Game) Your normal analysis actually is even more precise than the finite/infinite meta view you mention in the MSFT/AMZN comparison. Let’s look at it in the four quadrant frame- work that we normally use. MSFT is clearly still a Rock star while AMZN looks to have slipped to Icarus. Whether it is because AMZN is battling everyone or not i am not sure.

Tools better than models

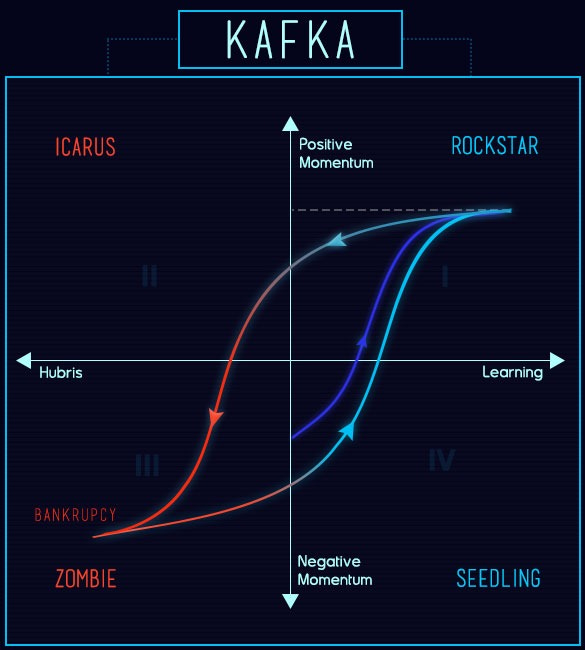

G.V: Agree, I see a clear need for tools to test our narratives. That is the reason Macrowise has built KAFKA, a tool that allows institutional investors to take advantage of the evolutionary nature of markets.

Macrowise KAFKA dashboard.

We both like to think about markets in terms of evolution. Paul Ormerod, In Why Most Things Fail, talks about the phenomenon that has been ignored by many economists and practitioners. Failure is something that has not been sufficiently analyzed and explained even by newer economic ideas such as game theory or behavioral finance. The only insight we have about failure comes from the science of biology, especially the study of extinction. Extinctions obey a power law. Large events may have very small causes. Species do not become extinct simply because of external shocks (such as the meteor that affected the dinosaurs); rather, extinction is built into the system.

As we have discussed many times together diversification based on correlation of asset classes, geographies or industries is completely ignoring this fact. Companies, like living beings, have an evolution process. Companies rise as startups, or begin as a great idea from founders. They have an idea of the future that could be true or not. There is a powerful and costly learning process where the founders learn how to create the right product-market fit and build the right team to deliver. At this stage, the company is a seedling, and develops a consistent learning process that cannot yet be reflected into the price action. Massive customer acquisition, unique value proposition and media attention help transform this Seedling into a Rockstar where price action is extremely positive. The management is narrowly focused and underestimates the changes in the dynamic of the business and the economy.

At some point in the process, a misfit between product and markets can occur despite the company’s continued positive price action. As an Icarus tries to reach the sun, the bubble burst when the market proves that the business model wrong. The Icarus reaches a very dangerous zone with three options: bankruptcy, to become a zombie subsidized by some governmental incentive, or embracing an internal process of creative destruction and reinventing of the company.

Following the quant insights of our tool, MSFT is in a Rockstar regime while Amazon is being recognized as an Icarus.

Jim lets have conversation #2 next month and we will explore the KAFKA tool in more detail.

Sincerely,

James Leitner and Guillermo Valencia.

Macrowise Founders

December 16th, 2019.

Links:

Why most things fail by Paul Ormerod