Get Ready For Volatility In The Eurozone

Bogotá, Colombia. Guillermo Valencia AOur structural trade in 2019 is being short globalisation and long localism.

The European Union has created many opportunities to express this trade.

The ECB (European Central Bank) has maintained their commitment to pressing the liquidity button within the Eurozone.

Negative interest rates have created a big rally in the DAX (German Equity Index) and the ECB rhetoric is that these negative interest rates have been positive for the economy overall.

Source: Stockcharts.com

Volatility has been compressed and the illusion of liquidity is hidden by two important factors: 1) Buybacks are decreasing the float. 2) The liquidity of the ETF industry is concentrated in just a few main actors.

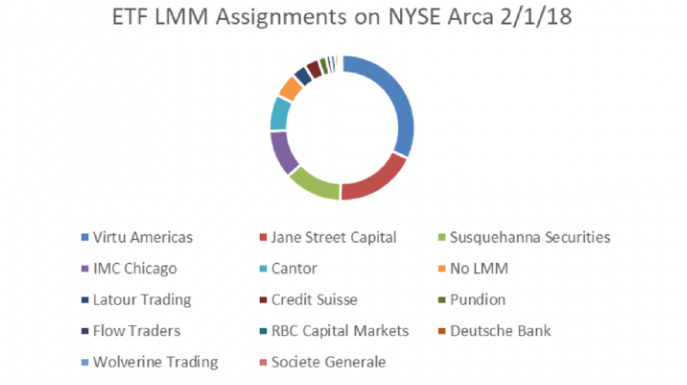

5 Market makers provide 87% of liquidity to the ETF markets.

Source: https://exponentialetfs.com/big-etf-risk/

For that reason we now have tremendous gaps in the equity markets. Don't forget the equation: dP=(D-S)/Liquidity where less liquidity in the market leads to higher price fluctuations. (P=Price, D=Demand, S=Supply)

While the speeches of central banks aim to bolster trust in the European economy, the European Renewal Manifiesto of President Macron shows that Europe is facing an imminent threat.

Nationalist retrenchment offers nothing; it is rejection without an alternative. And this trap threatens the whole of Europe: the anger mongers, backed by fake news, promise anything and everything.

What country can act on its own in the face of aggressive strategies by the major powers? Who can claim to be sovereign, on their own, in the face of the digital giants? How would we resist the crises of financial capitalism without the Euro, which is a force for the entire European Union?

The best way to see the European Paradox is by looking at the weakness of the Euro.

Source: Stockcharts.com

Italian Bonds are good indicator of the changing beliefs among investors, from strength to weakness in the Eurozone. Elections and the slowdown of global trade will bring further problems to the Eurozone.

Source: Stockcharts.com

Another way to play our view is by shorting Germany, a country highly dependent on exports, while being long a more internal consumption play, such as Brazil. If we make a ratio between the Brazilian ETF (EWZ) to the German ETF (EWG), the EWZ trade looks very promising after a general increase in volatility.

Source: Stockcharts.com