Investment is not just about return and volatility, but about growth and longevity.

Risk management is not just about diversification; it is about selecting assets, social contracts, and companies with a higher survival bias.

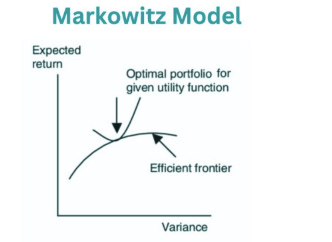

Conventional financial theory hinges on the principle of diversification, an idea popularized by Harry Markowitz. This theory suggests that a stock should be evaluated based on two attributes: return and volatility. Typically, volatility is seen as a measure of risk.

However, let’s shift our perspective. Companies aren’t just lottery tickets, as Peter Thiel mentions. They are living entities, driven by passionate founders and a committed management team with a clear purpose. The best companies often have groundbreaking products, and if they haven’t yet caught the market’s eye, they might be valued attractively.

Instead of focusing on return and volatility, we should consider a company's growth rate and its longevity. The crucial question isn’t about the volatility of an asset, but whether this company will still be thriving in the next 10 to 25 years. Will this country maintain its social contract over the next quarter-century? This is the kind of long-term thinking that Warren Buffett and Charlie Munger embrace when they buy companies with the intent to hold them indefinitely.

Survival changes everything. When we accept the fundamental law of impermanence, we realize that companies can fail, social revolutions can reshape economic systems, and empires can fall. This is why selection is far more critical than diversification. Risk management shouldn’t be about minimizing volatility but about avoiding investments in entities unlikely to survive the next 20 years. It should focus on those with a strong bias towards longevity, while also ensuring that extreme volatility doesn't eliminate you from the game.

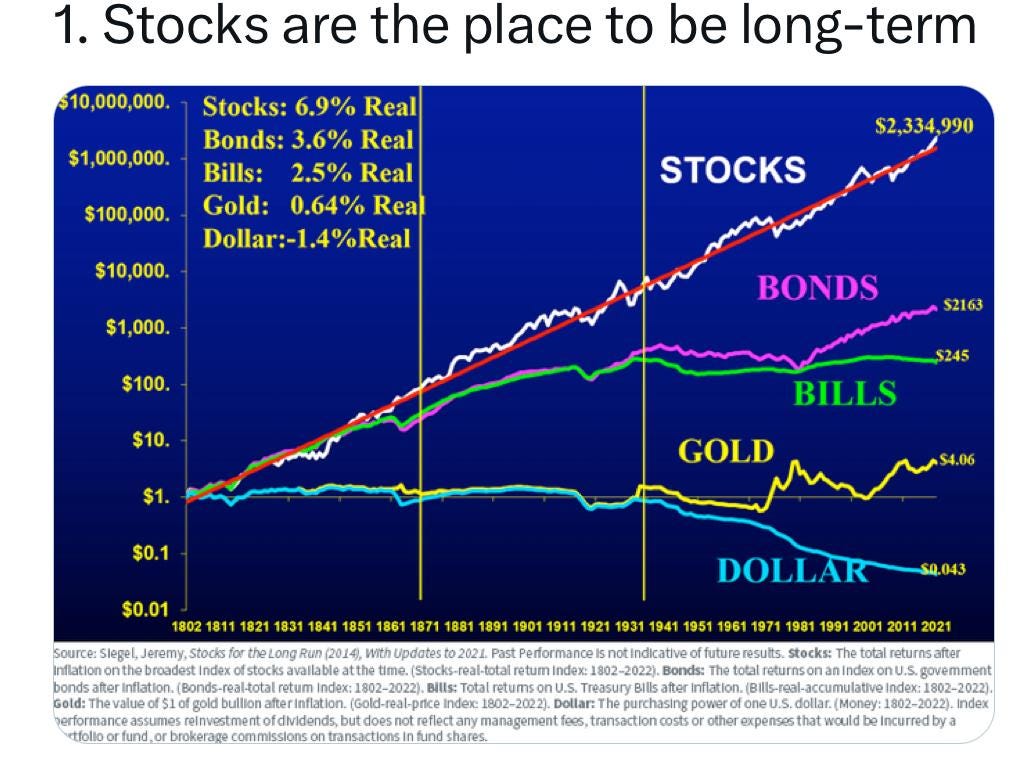

Consider the popular graph comparing investments in stocks, bonds, gold, and currency since 1800. The clear winner over the past 200 years has been U.S. stocks. In this period, our civilization has seen nearly nine generations, over 49 major revolutions, and 25 significant wars. The social contract of the United States has shown remarkable resilience. Despite challenges like the Civil War, it has endured. This is not the case for Napoleon’s France, Prussia, Weimar Germany, Tsarist Russia, the British Empire, or the Soviet Union.

The difficulty in maintaining a stable social contract is evident when we look at how often Germany has changed its currency: from the Kurantmark to the Euro, through various other iterations. And this is a country with significant technological and scientific development, not to mention the tumultuous monetary histories of countries like Argentina, Brazil, Turkey and other emerging economies.

Surviving is hard. Stocks have proven to be a better long-term bet than relying on the transient social contracts of the prevailing empires. When you delve deeper, you’ll see that within the world of stocks, success is often concentrated among a few big winners—those that define new production models for our society.

Concentration is natural !

Thanks for reading,

Guillermo Valencia A.

Cofounder of Macrowise

Bogotá, Colombia

June 9th, 2024