The AI Wars: Five Wars, One Machine

Artificial intelligence is not one race. It is five wars stacked on top of each other — energy, silicon, interconnection, models, and the humans and agents at the top —

Start with a shipping container in the high desert of New Mexico. Inside it, racked floor to ceiling, sit a few thousand graphics chips. They are not drawing graphics. They are multiplying numbers — trillions of them every second — and to do it they are drinking electricity and breathing out heat. Somewhere a transformer the size of a school bus is feeding the container more power than the town beside it.

Zoom out. That container is one cell in a building the length of an aircraft carrier. That building is one node in a fabric of buildings being wired together across three states, fed by power plants being built faster than at any time since the 1970s. The chips inside come from a single island off the coast of China, etched by a single machine made in a single town in the Netherlands. And the numbers those chips multiply will become a model — a mind, of a kind — that a billion people and an uncountable swarm of software agents will lean on to think.

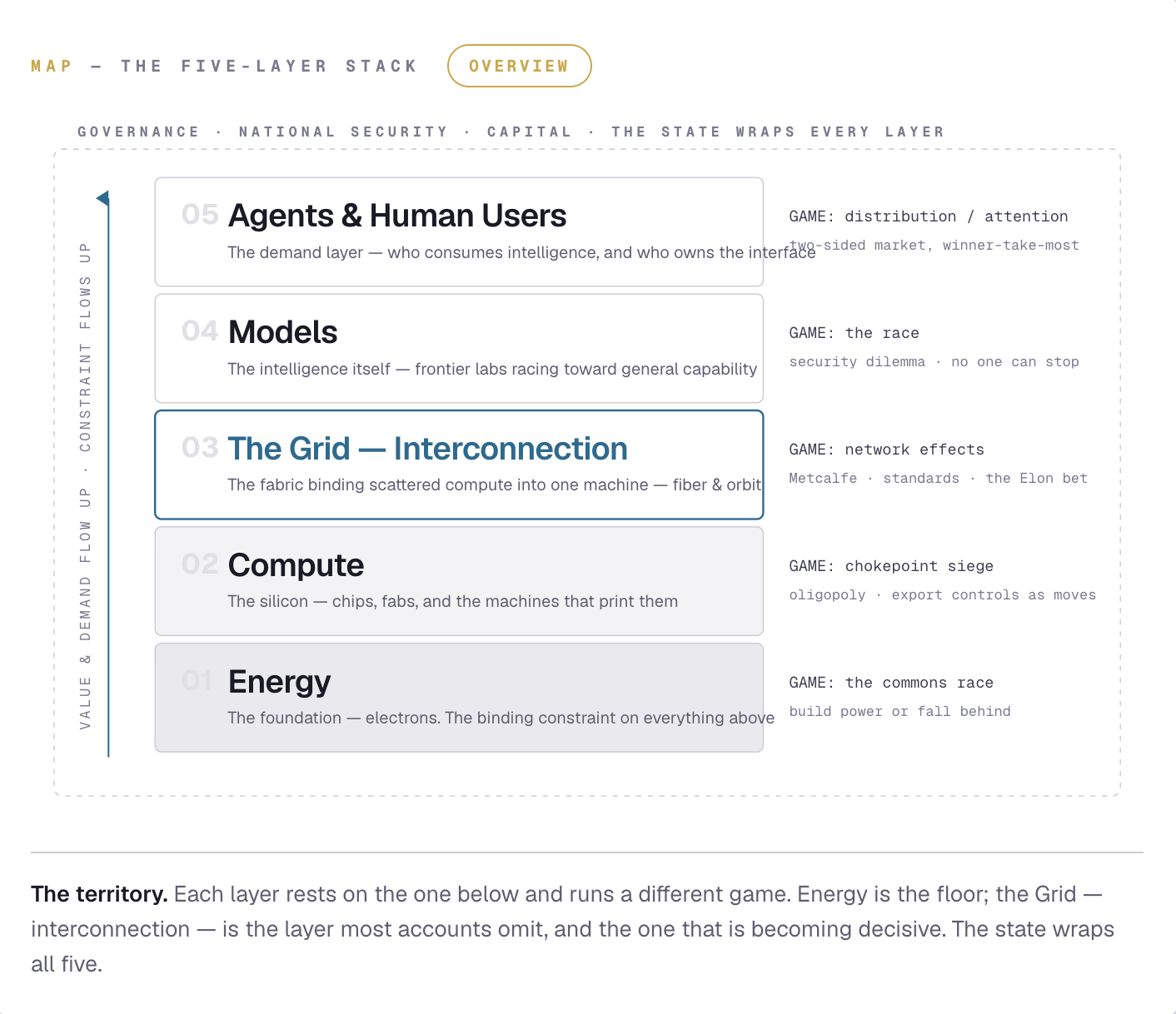

This is what people miss when they argue about “the AI race” as if it were one race. It is not. It is a stack of five separate competitions, each sitting on the one below it, each governed by a different logic. You cannot win the top without holding the bottom. And almost nobody holds all five.

So do the thing the vocabulary discourages: refuse to be impressed by it, and ask the dumb question. What is physically happening here? Strip away the press releases and intelligence — the artificial kind — is the act of turning energy into useful computation, then moving that computation to where it is needed. Joules in, predictions out, distributed across a network. Everything else is scaffolding around that single transaction.

If that’s the core, the war is over four scarce things — the energy that powers the computation, the silicon that performs it, the network that binds it into one machine, and the intelligence that results — plus a fifth war over who gets to use it. Five layers. Five games. In each I’ll ask the same two questions: the game-theory question (what is the strategic structure, and where does it settle?) and the network question (who are the nodes, and which connections, if cut, bring it down?). We climb the five layers one at a time; then we widen out — to the nations fighting over them, the companies playing the whole board, and finally the endgame all of it is bending toward.

But first, the law that governs all five. A simple race model — two players, one prisoner’s dilemma — is too blunt. The real stack has dozens of firms per layer, incomplete information, increasing returns, and tipping points. The right tool is the global game (Carlsson–van Damme; Morris–Shin): give each player a slightly noisy belief about which way the world is tipping, and the math collapses from “anything can happen” to a single outcome governed by a threshold, θ*. Below it, fragmentation. Above it, a cascade — and one winner takes the layer. Standards wars, platform tipping, bank runs, currency attacks: all the same engine. Here is the map, and the law.

Power cannot be downloaded. You have to build it, in the world, against the laws of the grid.

Energy: The War for Electrons

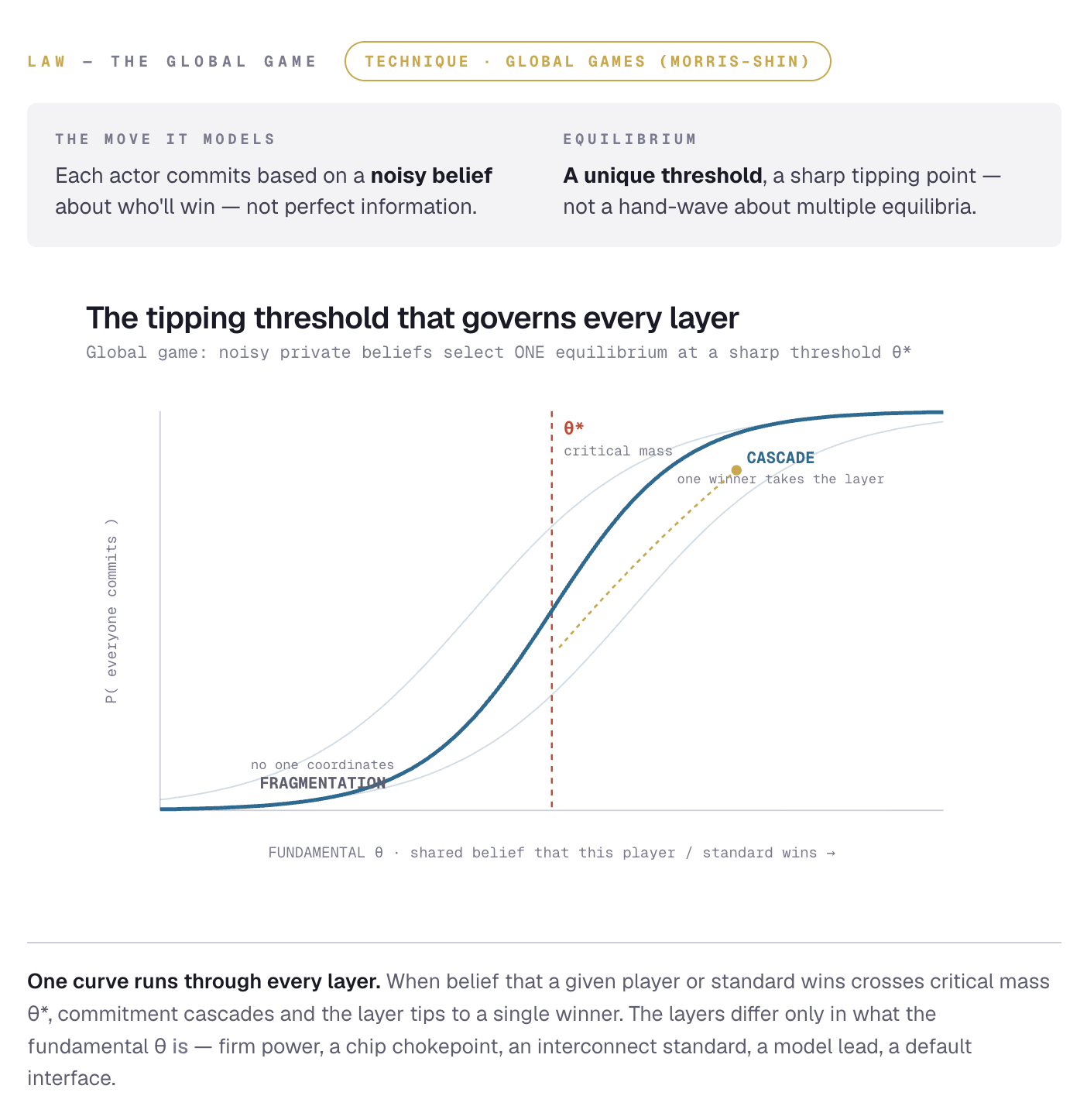

When a model answers you, what does it spend? Joules. A single frontier query can cost ten times the electricity of a web search; training a model can consume as much power over months as a small city. The intelligence is a thermodynamic event — somewhere a turbine spins so a sentence can be written. The bottleneck on AI is not cleverness, and in the long run not even chips. It is power: gigawatts of dispatchable electricity, delivered to one place, today. And power cannot be downloaded.

That makes energy a common-pool / congestion game. The grid is shared, and the queue to connect a new data center now stretches years. So the dominant strategy is to stop waiting in line — enclose your own generation, behind your own meter, co-located with the computer. That single move explains a flurry of headlines: a tech company restarting Three Mile Island; gas turbines sold out into the next decade; fuel cells with a hyperscaler waiting list. The smart players stopped sounding like software executives and started sounding like utility barons.

The board has ten serious actors: nuclear and gas incumbents (Constellation, GE Vernova, Vistra, Talen, Siemens Energy), on-site fuel cells (Bloom), SMR challengers (Oklo, NuScale), uranium (Cameco), and infrastructure capital (Brookfield). The network point is brutal: in a congested grid the scarce thing isn’t generation in the abstract, it’s generation connected to your node. Whoever locks up firm power next to buildable land has seized the high ground for the entire stack above.

Power cannot be downloaded. You have to build it, in the world, against the laws of the grid.

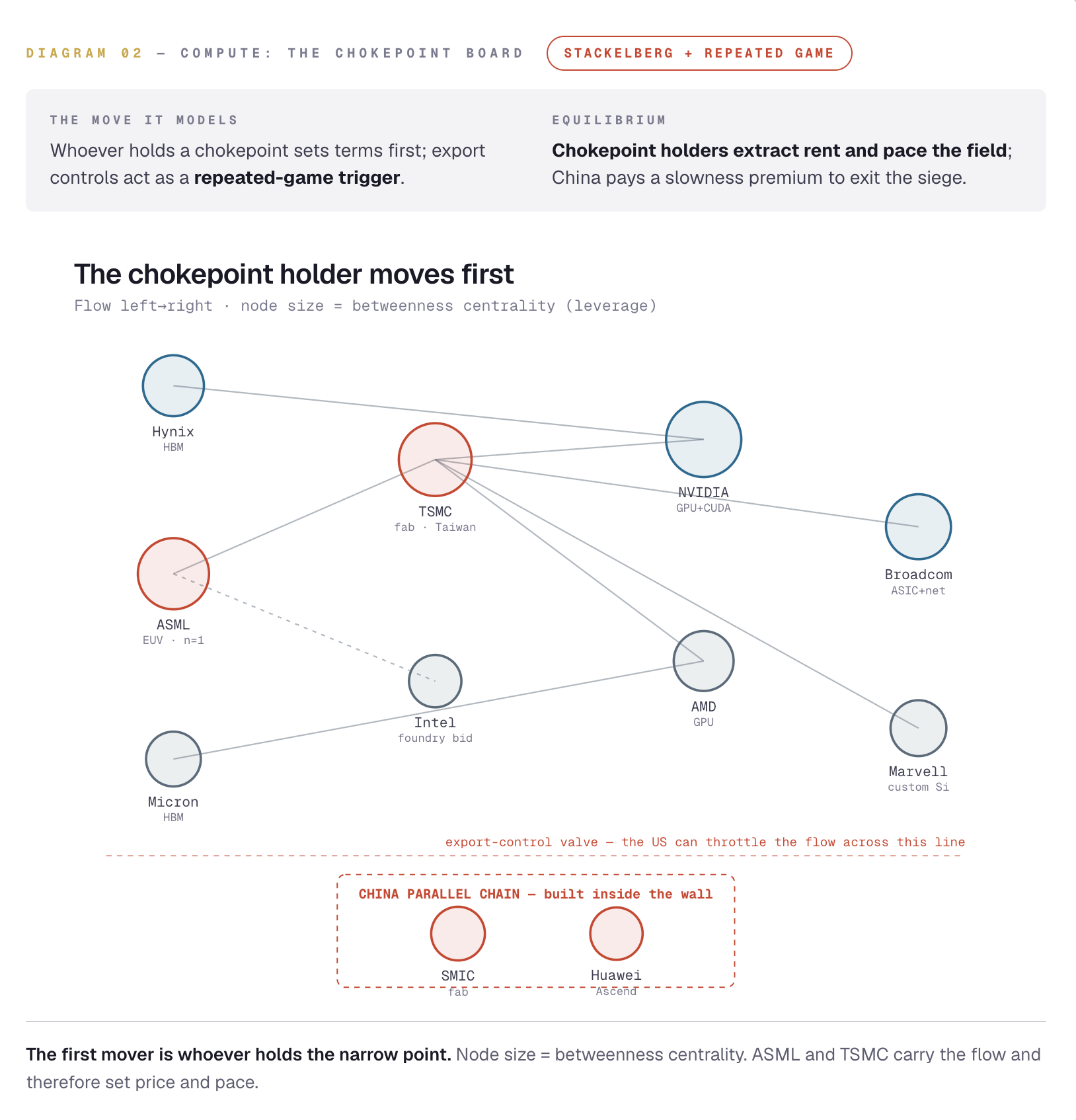

Compute: The War of the Chokepoints

A GPU is a machine for doing one boring thing — multiply, add — tens of thousands of times at once. Neural networks are, underneath, enormous piles of exactly that. The chip built to shade video-game pixels turned out to be the perfect engine for thought. Follow it backward and you find the strangest fact in the modern economy: the most advanced object we mass-produce runs on a chain of monopolies feeding monopolies. Designed by essentially one company (NVIDIA, whose real moat is the CUDA software everyone learned). Printed by essentially one (TSMC, on one island). Using a machine made by exactly one (ASML, in the Netherlands). No second source.

So this isn’t a symmetric race; it’s a Stackelberg siege — a leader–follower game played on a chokepoint and repeated, with export controls as the trigger strategy. The party holding the narrow point moves first and sets the terms. China’s countermove is the textbook response to a siege: build your own supply inside the walls — slower, costlier, but a determined state will pay almost anything to remove a hand from its throat. The board: ASML and TSMC (chokepoints), NVIDIA (the leader), AMD, Broadcom and Marvell (followers), SK Hynix and Micron (HBM), Intel (re-entry bid), and SMIC + Huawei (the parallel chain).

Network theory names the leverage: the node with the highest betweenness centrality — the one the most paths run through — is both most powerful and most fragile. ASML and TSMC have near-maximal betweenness in the most important supply network on Earth. That is why an island the size of Maryland is the most strategically sensitive real estate in the world.

The most advanced object we mass-produce runs on a chain of monopolies feeding monopolies.

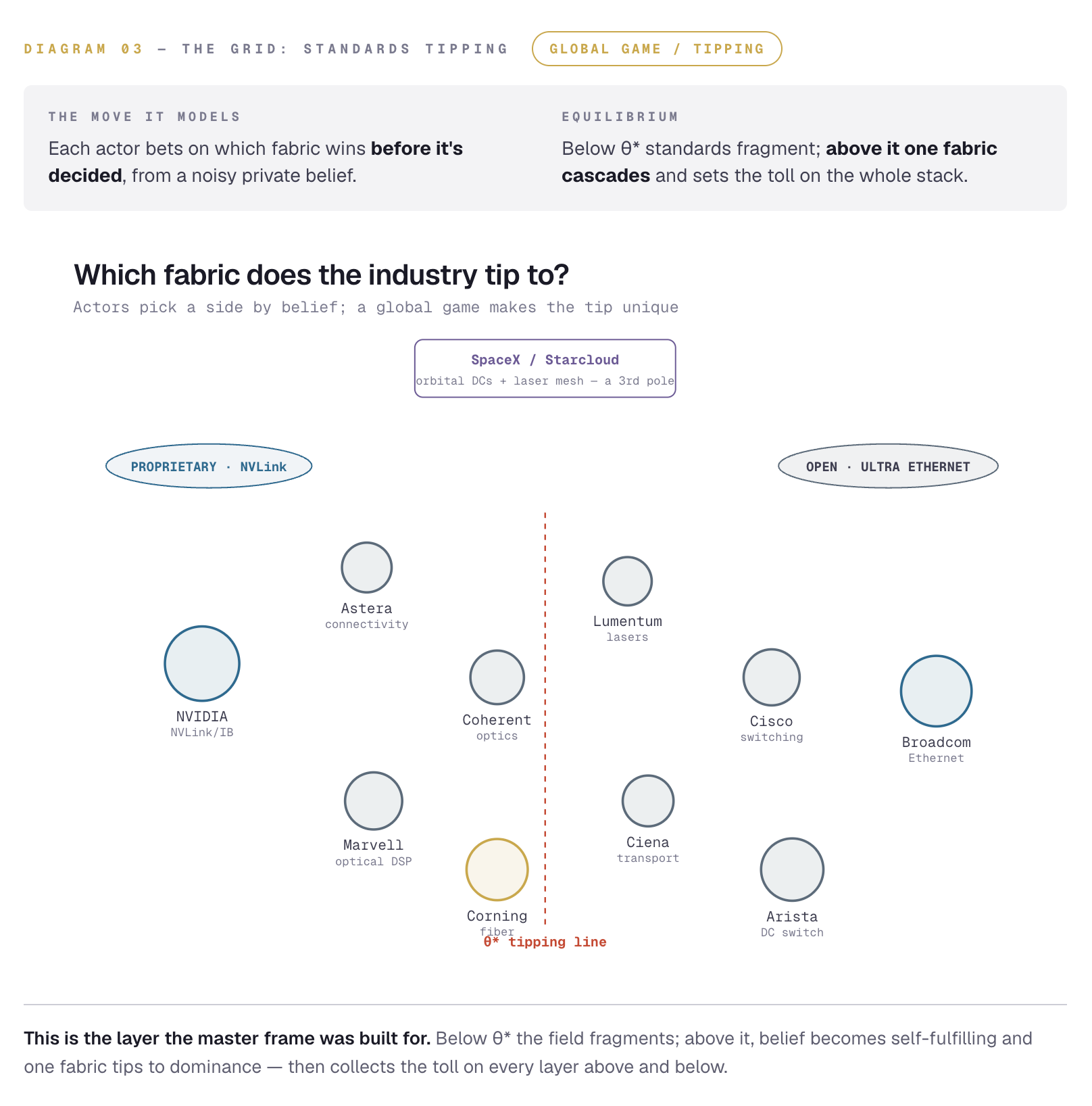

The Grid: Wiring the Machine Into One Mind

Here is the layer left out of almost every popular account, and the one I think will decide the most. Not the electrical grid — the interconnection grid: the cables, switches, and links that bind scattered silicon into a single computer. When you train a frontier model you don’t use one chip; you use tens of thousands, and they must behave as one machine. They’re a rowing crew — if the chips are the rowers, the network is the timing of the stroke. A crew of giants who can’t synchronize is slower than a crew of children who can. The dirty secret of large-scale AI is that the bottleneck is frequently not the chips but the wires between them.

Stack a constraint on a constraint: one site can only pull so much power, so the largest runs already exceed what a single campus can feed. The only way forward is to spread compute across many buildings, many regions — and bind them back into one logical machine across distance, fighting the speed of light. This is the context for the strategy that sounds like science fiction: put the data center in orbit, where the sun never sets, there’s no permitting fight, and you radiate heat into the cold of space. The same player has already flown the largest laser-linked satellite mesh ever built — the heritage tech for binding orbital and terrestrial compute into one fabric. The vision isn’t “computers in space.” It’s to own the interconnection layer itself, the grid everyone else has to plug into.

Why is owning it so valuable? Metcalfe’s Law: the value of a fabric rises with the square of what’s connected to it. That’s increasing returns — the grid that pulls ahead becomes the default, which lets it set the standard, and standards are toll booths. Which makes this the literal global game: ten actors — NVIDIA’s proprietary fabric (NVLink/InfiniBand) versus open Ultra Ethernet (Broadcom, Arista, Cisco), the optical suppliers (Corning, Coherent, Ciena, Lumentum, Marvell, Astera), and the orbital wildcard (SpaceX/Starcloud) — each betting on which fabric wins before it’s decided. Cross θ* and one cascades.

One actor is hiding in plain sight on this layer: the telcos. They already own the unglamorous physical grid — fiber routes, edge sites, spectrum, rights-of-way, the last mile — the exact assets an AI fabric needs. Most are asleep on it. The exceptions are instructive, and they tend to be run by one kind of founder. Masayoshi Son turned a Japanese telco into the spine of the buildout: Arm supplies the compute IP, the Stargate venture the energy and data centers, an OpenAI stake the model. In Korea, SK’s Chey Tae-won is pivoting SK Telecom into AI infrastructure while SK Hynix feeds it memory; in India, the Ambanis are wiring Jio’s vast subscriber base to NVIDIA-filled data centers. The telco that grasps that interconnection is the product, not the pipe, can leap a layer. Most won’t.

If the chips are the rowers, the network between them is the timing of the stroke.

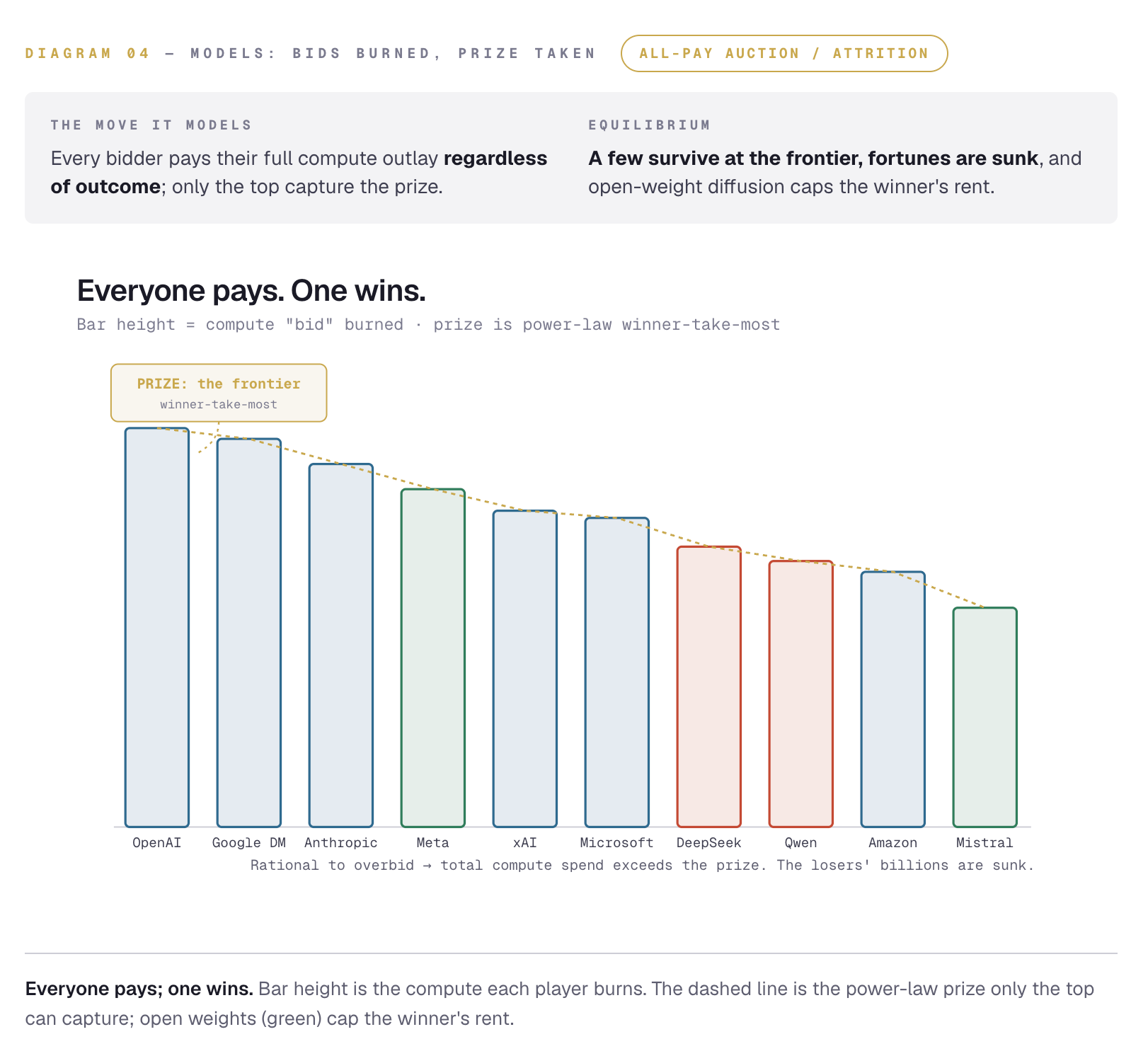

Models: The Race No One Can Quit

A model, stripped to the bone, is compressed prediction. Show a system enough of what humans have written and trained it to guess the next piece, and past enough scale it stops parroting and starts to generalize — it builds a rough working model of how the world hangs together. The engine is the scaling laws: more compute and data yield predictably better models, which converts a research problem into a spending problem. The newest gains come from letting models think longer and act as agents; the deepest prize is a model that helps design its own successor, where the curve stops being a curve and becomes a cliff.

The prisoner’s dilemma I started people with misses the cruelty here. This is an all-pay auction — a war of attrition — where every bidder pays their compute whether they win or lose, and the prize is power-law. So it’s rational to overbid, and aggregate spend exceeds the prize: pure dissipation. Overlay the security dilemma and you see why “just slow down” keeps failing — unilateral restraint is ruinous, so everyone races to the outcome no one chose. The board: OpenAI, Google DeepMind, Anthropic and xAI bidding hardest; Meta, Mistral, DeepSeek and Qwen changing the game by giving the weights away; Microsoft and Amazon hedging.

The network twist: talent and capital obey preferential attachment — rich-get-richer — which concentrates the frontier toward a handful of labs. The counter-force is open weights, which diffuse capability downward and cap how much rent the winner can extract. So the layer is a standing tension: relentless concentration at the very top, relentless diffusion just below it.

Everyone pays. One wins. The losers’ billions are sunk.

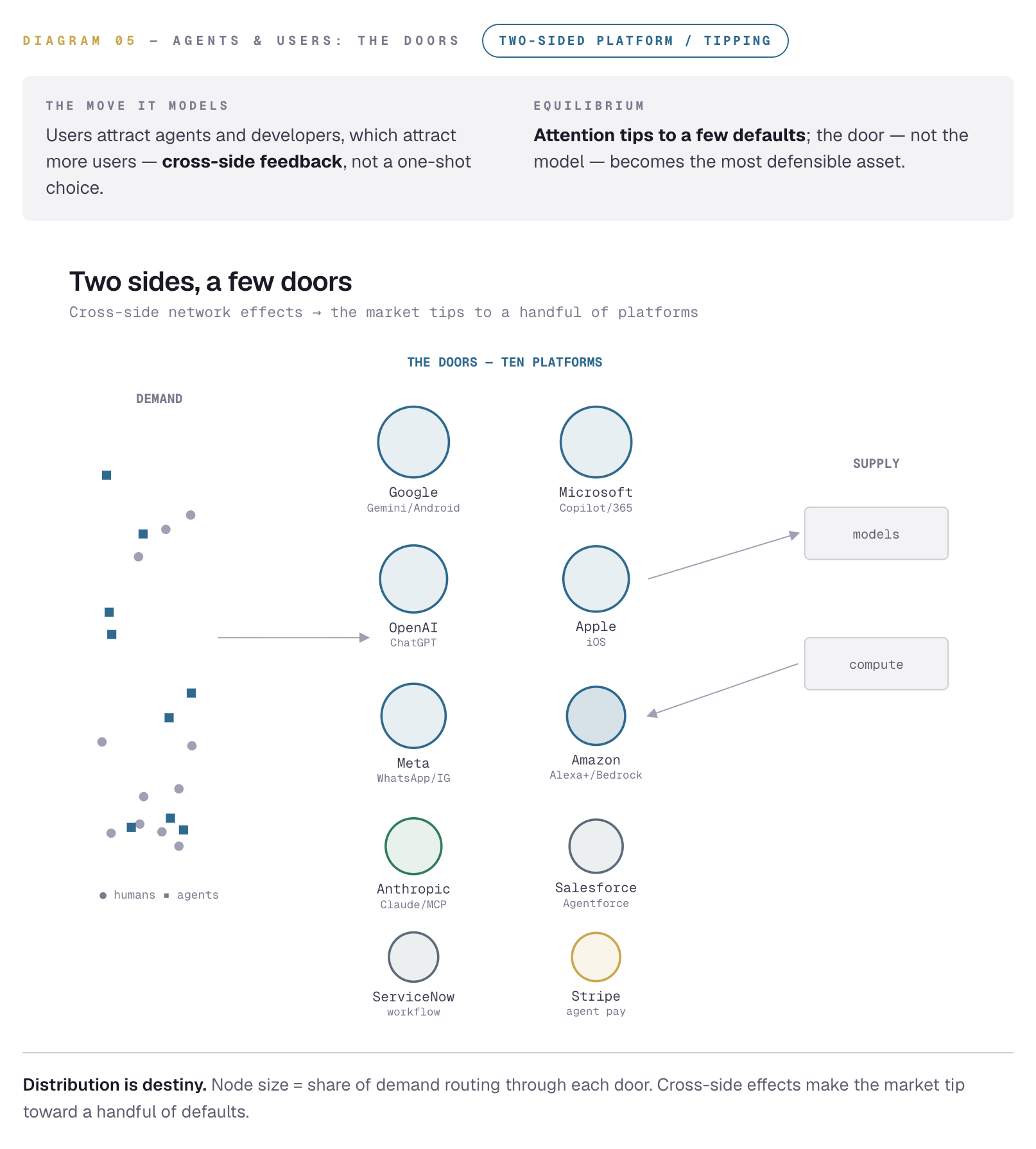

Agents & Users: Who Owns the Door

Who actually uses this intelligence? For a few years: people, a billion of them typing into chat windows. But the answer is changing under our feet. Increasingly the users are agents — programs that call a model, then call another program, then another agent, chaining actions without a human in the loop. The fastest-growing population on the internet is non-human. And that matters for one reason: distribution is destiny. Whoever owns the door — the default assistant in the phone, the OS, the suite, the enterprise workflow — decides which model answers, which compute runs it, which energy powers it. The bloodiest fights aren’t about who has the smartest model this quarter; they’re about who owns the default.

A new layer is crystallizing in real time: the agent grid. When agents call agents they form their own network, which raises the interconnection questions one floor up — how do agents discover each other, establish trust, and pay, machine to machine, at machine speed? Whoever sets that protocol owns a toll booth on the agent economy. Watch the quiet work on agent identity and payment rails; that’s where a future chokepoint is being poured like wet concrete.

Game-theoretically this is a two-sided platform market, and platform markets tip. The ten doors — Google, Microsoft, OpenAI, Apple, Meta, Amazon, Anthropic, Salesforce, ServiceNow, and the agent-payment rail Stripe — compete for cross-side network effects: more users pull more agents and developers, which pull more users. A handful capture most of the flow. The door, not the model, may be the most defensible asset in the entire war. And these agents need not stay virtual: humanoid robots and autonomous fleets are embodied agents — software that acts on the physical world — which is the bet behind Tesla’s Optimus and robotaxi programs.

And there is a quieter door — the one that decides the enterprise and the agency: the context layer. A raw model knows everything in general and nothing about your institution — your data, your permissions, the actions you are allowed to take. Whoever owns the connective tissue between the model and that operational reality owns something stickier than any model. Palantir is the purest bet on it: its Ontology is a living map of an organization’s objects, relationships, and permitted actions, and the platform stays deliberately model-agnostic — plug in whoever is best this quarter. The flywheel is the tell — the system improves not because the model grows but because the context deepens. Models commoditize; context compounds. Own the ontology and you own the seam where intelligence becomes action.

The fastest-growing population on the internet is non-human. Whoever owns the door routes them all.

Why This Is a National Security Question

Step back and you see why governments stopped treating AI as a tech-sector story. Intelligence is the master technology — it improves every other thing: weapons, biotech, cyber, productivity, even intelligence-gathering itself. And unlike electricity or the printing press, it can be turned on the problem of improving itself. That gives states three reinforcing reasons to panic: military (autonomy, cyber, the speed of decision, almost all dual-use), economic (whoever leads captures the productivity frontier), and the vertiginous one, strategic surprise (a self-improving lead could harden into a decisive, unassailable edge — and no state can afford to be wrong about that once).

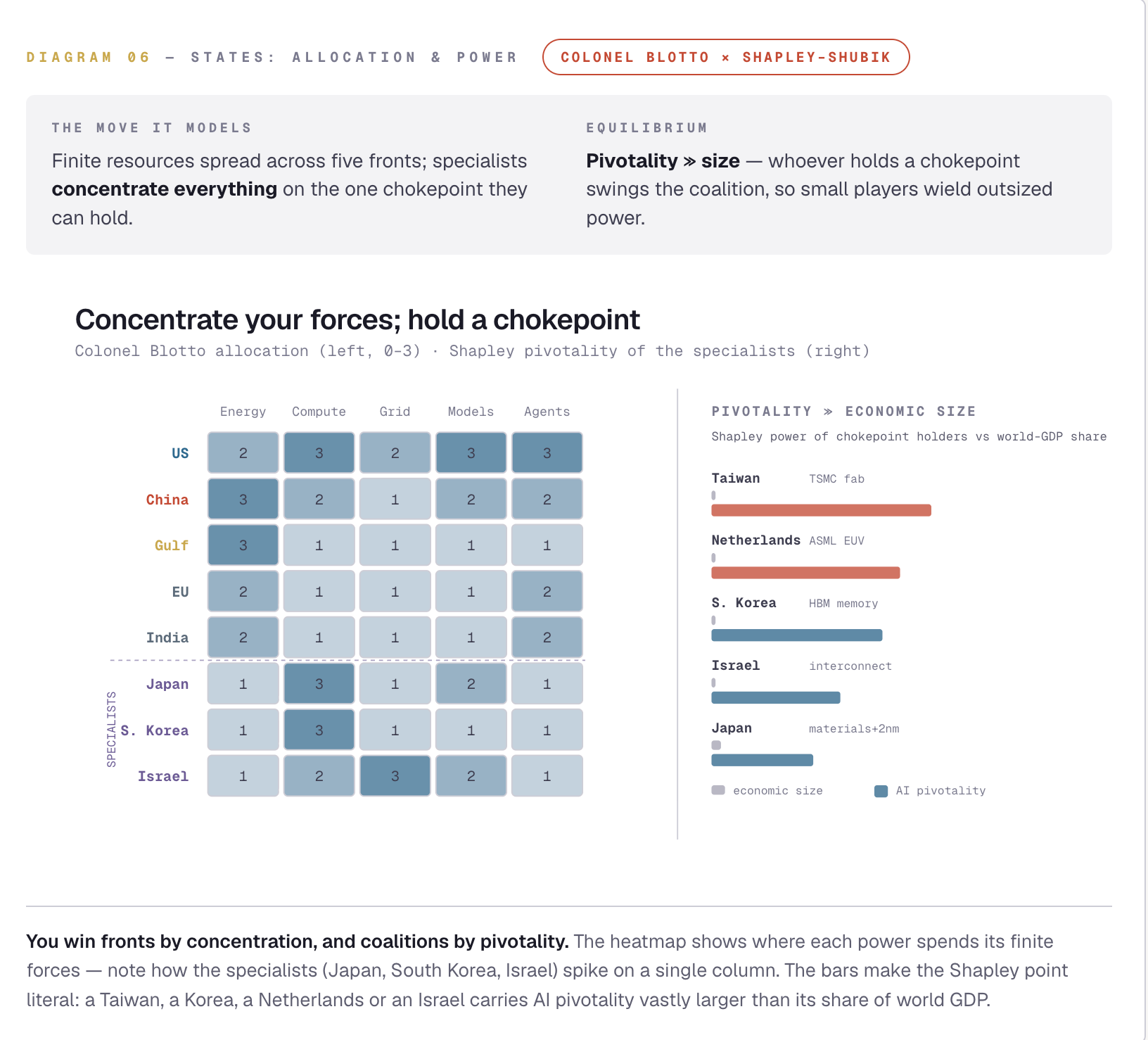

So the state reaches into every layer: it subsidizes energy and fast-tracks reactors, weaponizes compute through export controls, funds and secures the model labs, and treats the demand layer as sovereign territory. “Sovereign AI” is the phrase of the moment because every serious country now wants its own slice of the full stack. The right tools here are two. Colonel Blotto: each power has finite resources to spread across five fronts, so it cannot lead everywhere and must concentrate. And Shapley–Shubik: power isn’t size, it’s pivotality — whoever holds a chokepoint can swing the winning coalition, so their index exceeds their footprint.

And not every winner plays for the whole board. The sharpest national strategies are specialist — own one indispensable layer so completely that everyone, friend or rival, must come to you. South Korea is the memory chokepoint: Samsung and SK Hynix make roughly nine in ten of the world’s high-bandwidth memory chips, and not a single AI GPU runs without them — SK Hynix has sold its entire 2026 output in advance. Japan is rebuilding a second source to Taiwan — the state-backed Rapidus is a $16-billion moonshot to make 2-nanometer chips on home soil by 2027 — while quietly holding the materials chokepoints (the photoresists and ultrapure silicon almost no one else can make) and, through SoftBank, much of the capital. Israel is the interconnect brain: the technologies that bind thousands of chips into one machine — InfiniBand, NVLink, Spectrum-X — are largely architected at NVIDIA’s Israeli campus, the old Mellanox, alongside a defense-and-cyber AI complex and a startup density no country matches per capita. None of the three composes the full stack. Each is, in Shapley terms, pivotal — and pivotality is power out of all proportion to size.

A temporary edge could harden into a permanent one. No state can afford to be wrong about that, even once.

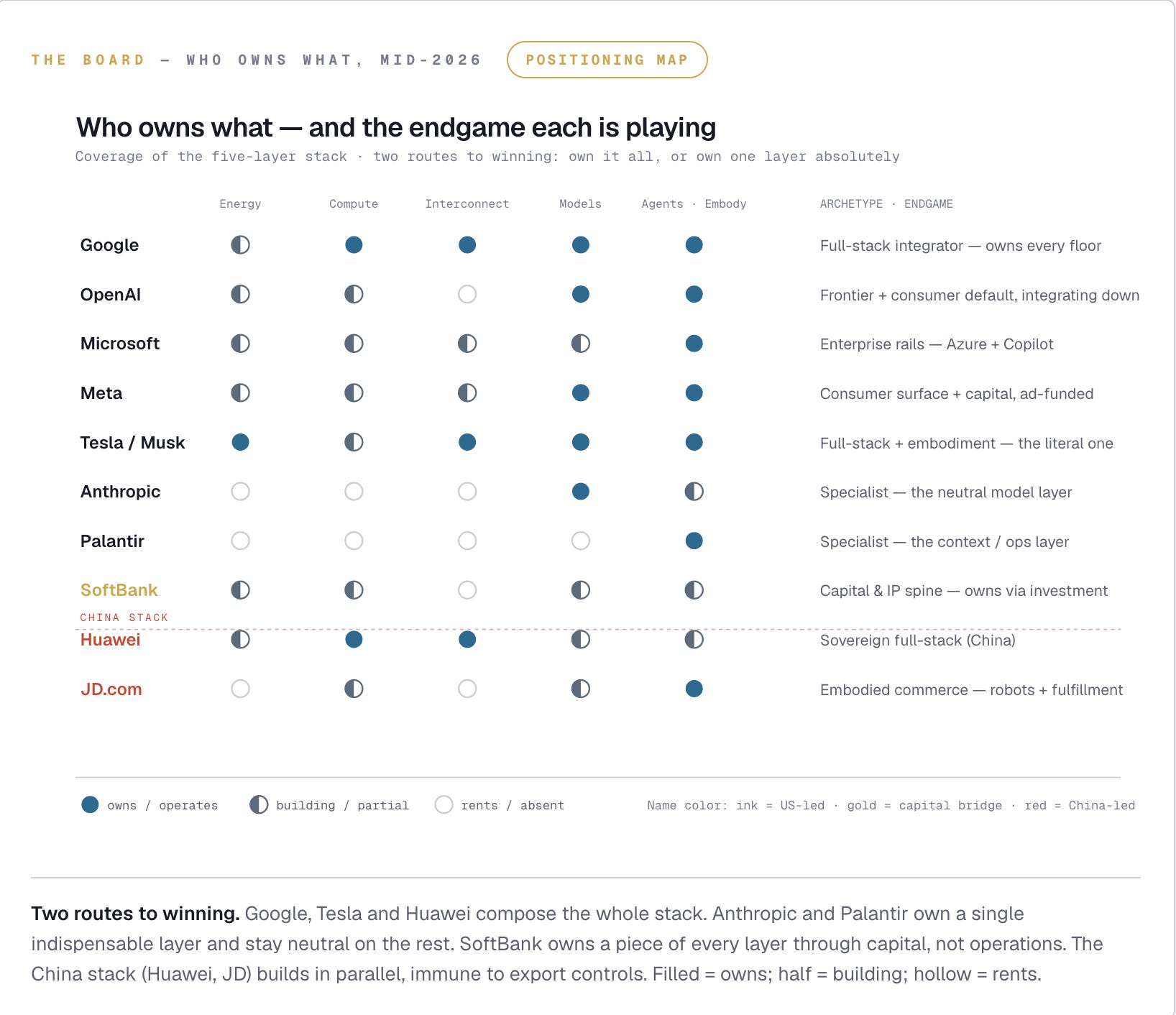

Who Owns What — and How They Win

So much for the layers and the nations. Now the firms. A company’s whole strategy reduces to one question: which floors of the stack does it intend to own? Plot the ten serious players against the five layers and the noise resolves into a picture. Two routes win — compose the entire stack, or own a single layer so completely you can’t be bypassed. Everyone in the muddy middle, renting every floor and owning none, is playing to lose.

The full-stack integrators. Google is the most complete entity in the field — its own TPUs, DeepMind, subsea fiber, energy deals, and the Android-Chrome-Workspace doors — and it sells TPUs to rivals besides. Tesla/Musk is the most literal, and the only one whose top layer is a body: Optimus and a robotaxi fleet. Huawei is the sovereign version, composing a China stack that export controls cannot reach.

The frontier-and-distribution players. OpenAI owns the consumer default and is integrating downward into its own chips and gigawatts; Microsoft owns the enterprise rails (Azure, Copilot) and is quietly loosening its dependence on OpenAI; Meta owns the largest consumer surface on Earth and is buying its way to the frontier, funded by ads.

The layer specialists. Anthropic refuses to own energy or chips and instead is the neutral model that runs on every cloud — power through indispensability, not integration. Palantir owns the context layer, the ontology where a model meets an institution’s reality. Both bet that owning one seam absolutely beats owning many shallowly.

The capital spine and the embodied play. SoftBank owns no layer outright but a piece of all of them — Arm’s IP, the financing behind Stargate, a stake in OpenAI — the closest thing the buildout has to a central bank. And JD.com is the quiet one: it already owns warehouses, fleets and the commerce graph, so its AI is embodied from day one — robots in the aisles, agents that actually fulfill.

The Seam Is the Prize

Go back to the container in the desert, knowing what you now know. It is not a computer. It is a cross-section through all five wars at once. The electrons feeding it were fought over in the energy layer. The chips inside passed through the chokepoints of compute. The cables leaving it are the front line of the grid. The model it trains is a move in the race. And the billion people and trillion agents who lean on that model are the prize at the top.

Here is the conclusion that took longest to see, and the reason both halves of this analysis — the physics and the game theory — point the same way. The five wars are distinct, but the players who win are not fighting inside one layer. They fight in the seams between layers. And that winning move — vertical integration across the whole stack — shows up at two levels at once.

The countries. A great power composes all five layers under one flag: energy policy, a compute supply chain, an interconnect, model labs, and sovereign distribution. Control of a chokepoint lets you build a bloc, so the world fragments toward two competing stacks, with the rest of the planet as contested nodes pulled by the same preferential-attachment gravity that concentrates everything else. An AI splinternet — two machines, two spheres, one long standoff.

The winner is the integrator — the country, and the company, that composes the whole stack.

Thanks for reading ,

G