The Macro Detective

Markets are selling off and the obvious suspect is liquidity. The obvious suspect is wrong. This is not a crisis. It is the market discovering the bottlenecks of the next civilization.

The case in one paragraph.

Bitcoin is falling. Gold, silver, and copper are surging. Credit is healthy and volatility is asleep. Read together, these are not the fingerprints of a liquidity drain — they are the fingerprints of a liquidity rotation. Money is leaving the dollar-speculative complex and the optimized export economies, and flowing into the physical bottlenecks of a new industrial era: energy, metals, networks, compute, and — least understood of all — robots. The regime has changed. We have left Globalization and entered Cold War II: a competition to define the dominant designs of AI, robotics, electricity, and monetary power. In that regime, rates are structurally higher, equities still rise, and the volatility is not noise. The volatility is the map.

Now the investigation.

The body: a death that isn’t one

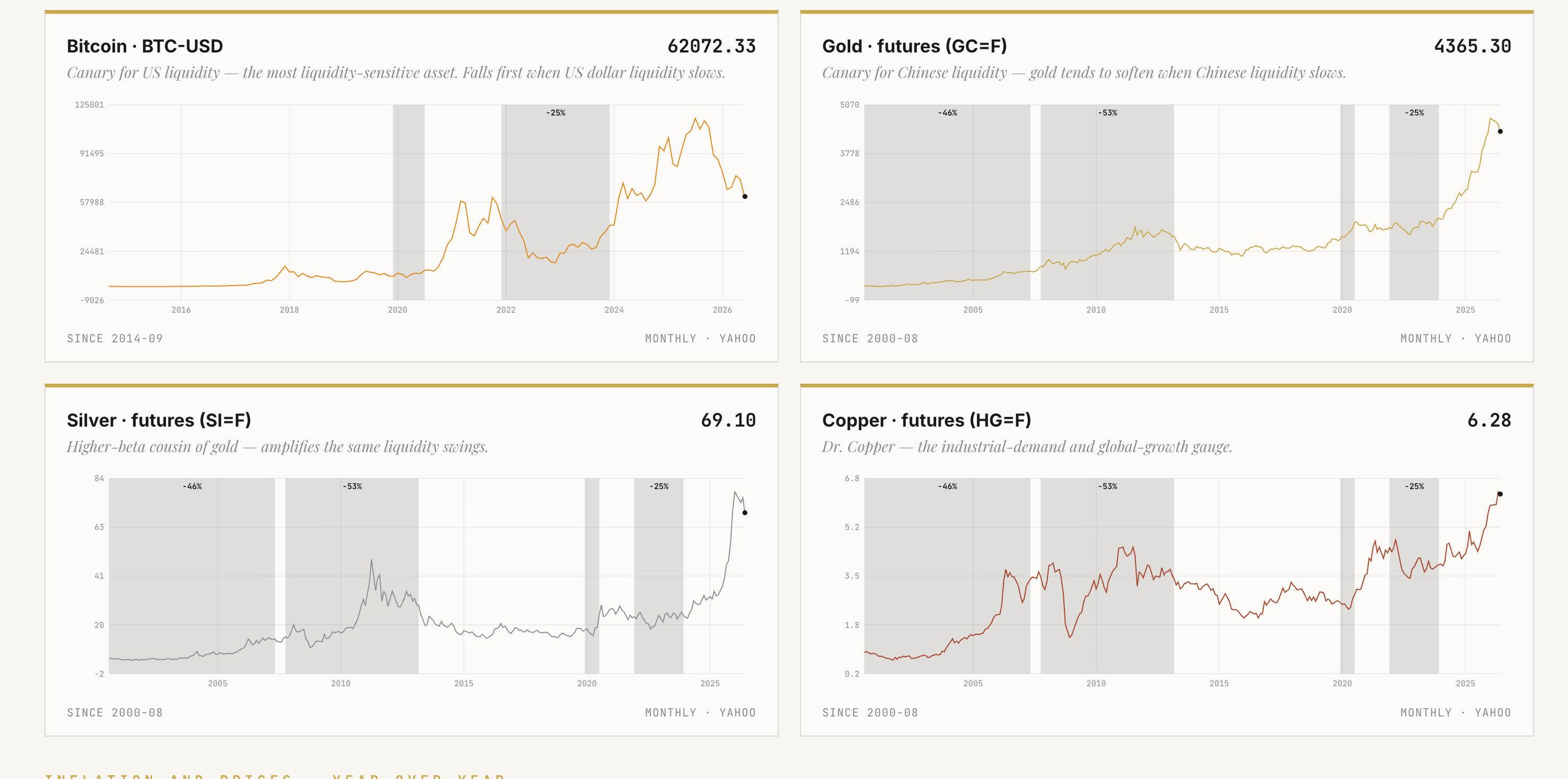

Start with the corpse. Bitcoin has rolled over hard, down to 62,072 from its highs. That matters, because Bitcoin is the most liquidity-sensitive asset we own — the canary for US dollar liquidity, the first thing to fall when the dollar plumbing tightens. So the dollar system is narrowing.

But walk three feet to the right and the scene refuses to cooperate. Gold is at 4,365. Silver — gold’s high-beta cousin, the asset that amplifies every liquidity swing — is vertical at 69.10. Copper, the metal with a PhD in global growth, is pressing 6.28.

A liquidity crisis kills these together. Instead, one canary is down and the others are climbing. That single divergence reframes the entire case: this is not money disappearing. It is money moving.

There are two liquidity systems here, not one. Bitcoin reads the dollar. Gold and silver read Chinese liquidity and the global hunger for hard money. They are splitting apart because they are measuring two different forces — and the gap between them is the case.

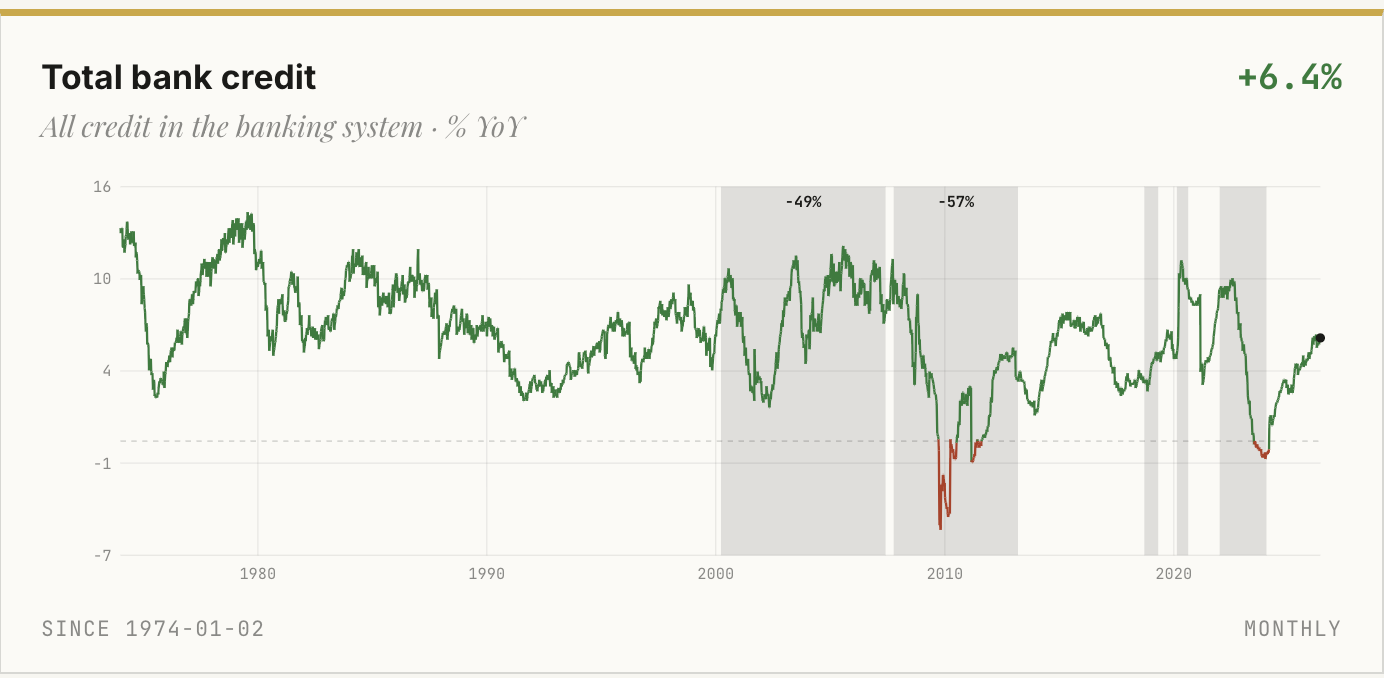

The alibi: credit is alive

Before chasing the money, rule out the catastrophe. If this were a real liquidity crisis, credit would seize first. It hasn’t.

Total bank credit: +6.4% year over year.

Loans to businesses (C&I): +7.7% — firmly expansionary.

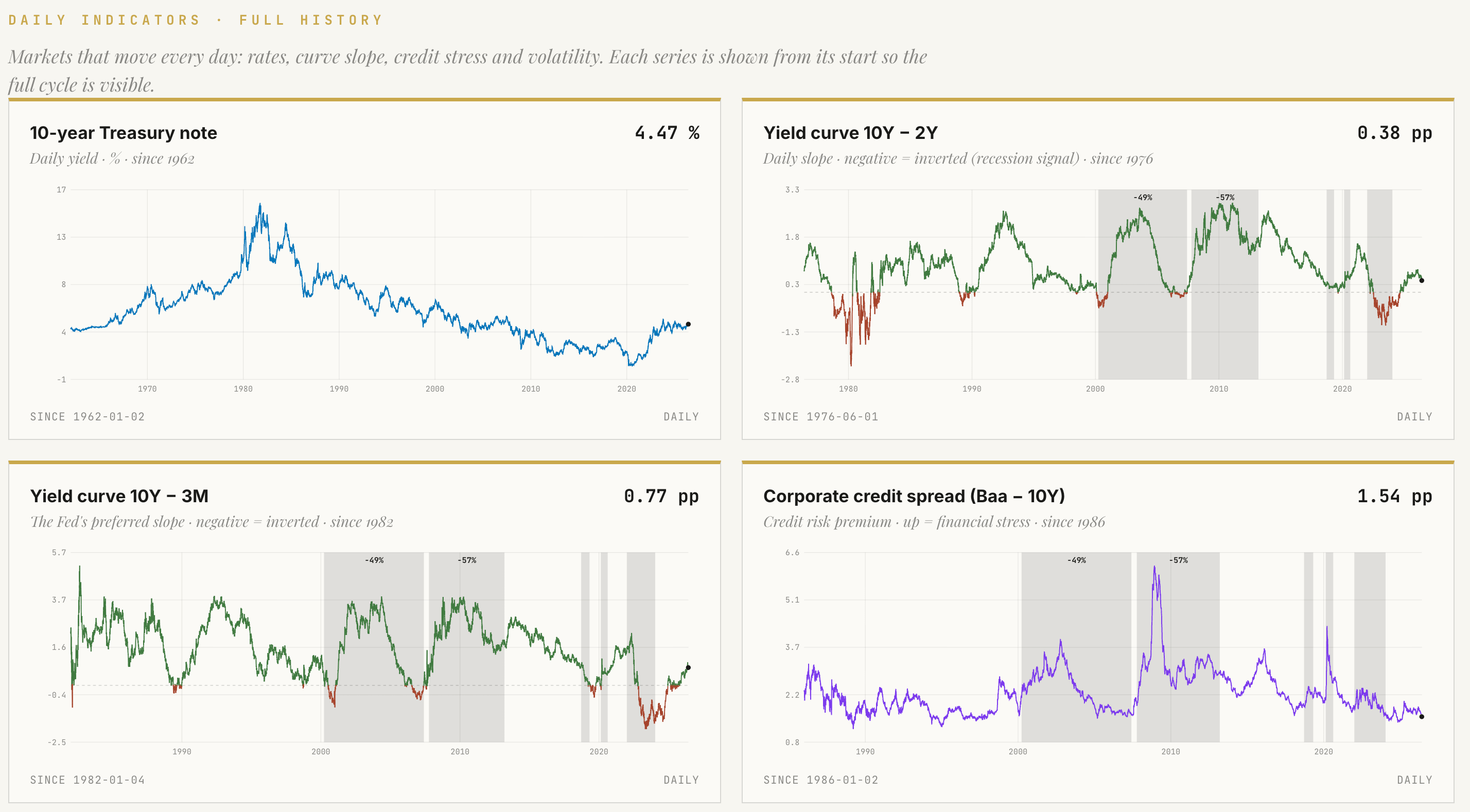

Corporate credit spread (Baa − 10Y): 1.54 pp, against a historical median of 2.14. That is the 8th percentile of financial stress in the entire history of the series.

VIX: 15.40 — also near its 8th percentile. Median is 18.

Read those percentiles slowly. The market’s stress gauge and its fear gauge are both nearly as calm as they have ever been. And the yield curve, which spent years inverted whispering “recession,” has un-inverted and re-steepened: 10Y − 2Y at +0.38, 10Y − 3M at +0.77. Both positive.

The body has a pulse. A calm one. So we are left with the only question that matters: where is the money going?

Follow the money: long the exporters, short the importers

Copper at 6.28 and WTI crude up +64.3% year over year are not subtle. Dr. Copper does not rise into a contracting world, and a 64% jump in the energy impulse is not demand destruction. The money fleeing financial speculation is landing in the physical economy.

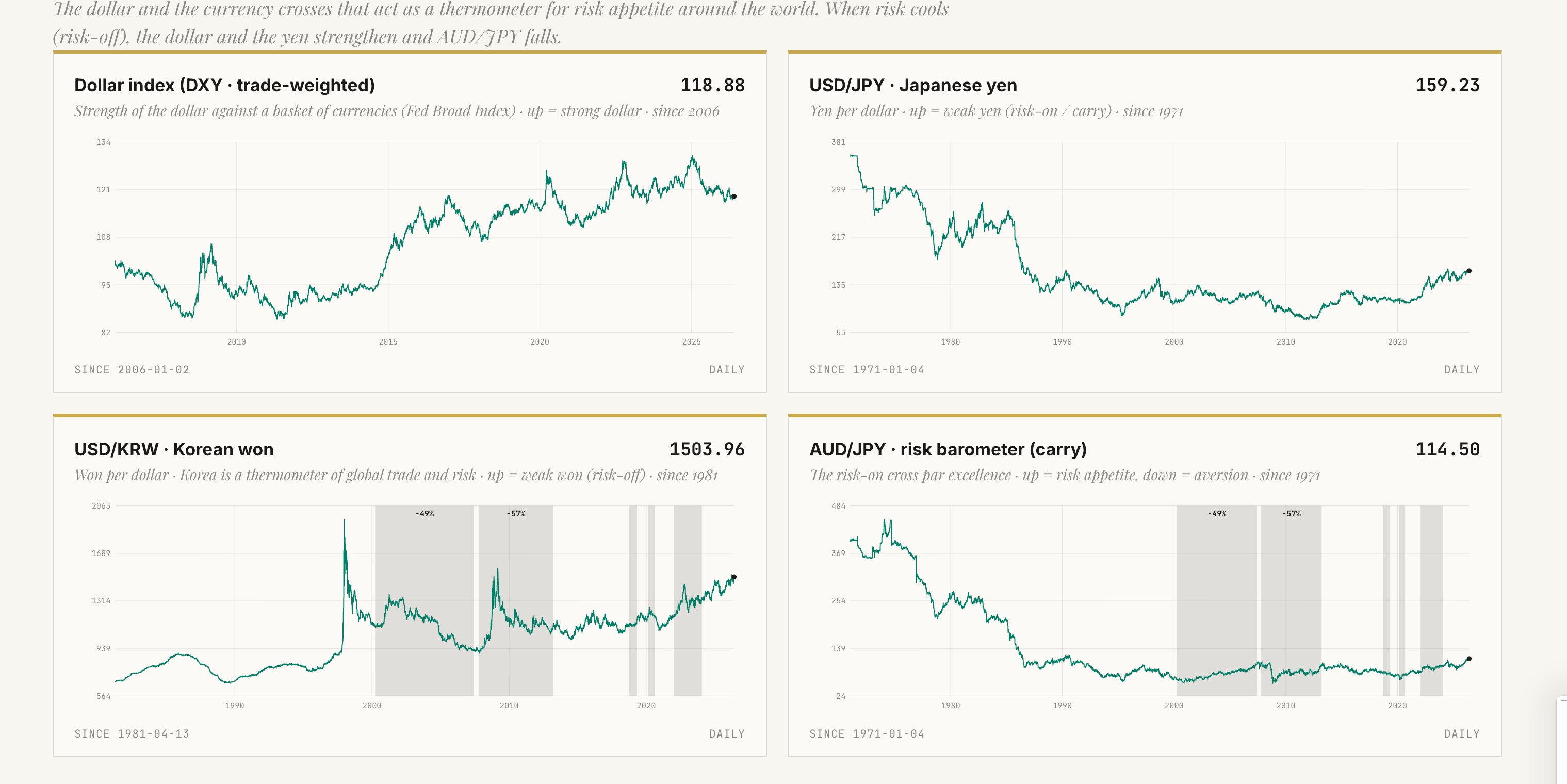

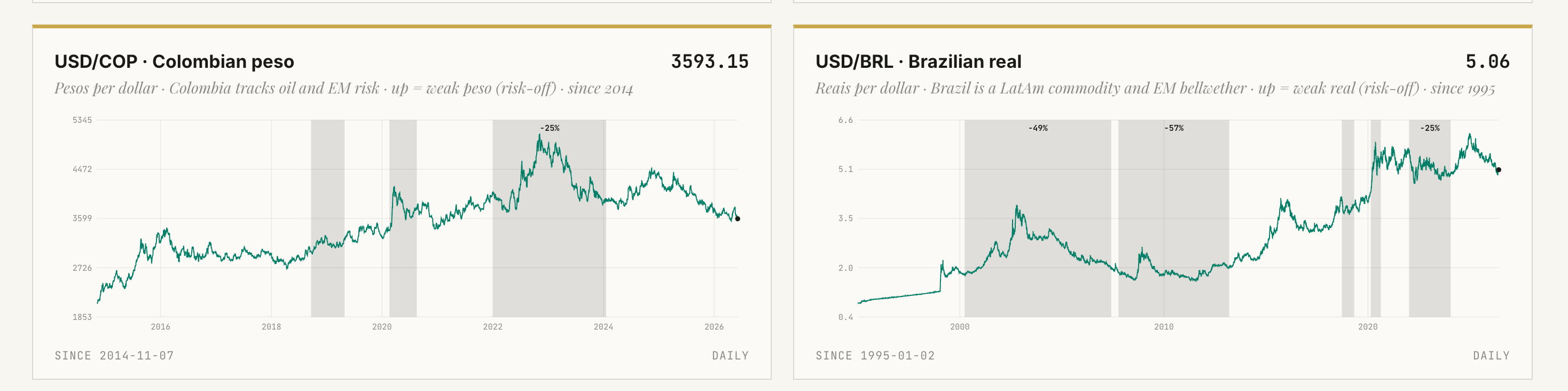

The currency board confirms it — and resolves into one clean, tradable axis. The dollar is strong at 118.88. The yen is weak at 159.23. The Korean won has blown out to 1,503.96.

Most analysts call this “EM versus DM” and move on. They miss the real fault line: energy exporters versus energy importers.

Japan and Korea are the purest energy importers in the developed world. Japan buys over 90% of its energy abroad; Korea imports roughly 84% of its primary energy and nearly all of its fossil fuels. They are also the heart of the semiconductor complex. That is the trap: they sit at the most critical choke point of the AI buildout, fabricating the silicon everything depends on — yet they must buy their energy on the open market. With crude up 64%, their terms of trade decay from both ends. The currency is the release valve, and it is venting.

The exporters are the mirror image. Colombia, Brazil, Norway sell into rising terms of trade. Every tick of the crude curve and every ton of copper is a tailwind to their currencies, not a tax.

So the divergence is not noise, and it is not abstraction. It is a position:

Long the energy exporters. Short the energy importers. The semiconductor importers are the squeezed cohort — indispensable to the next era, and penalized by it at the same time.

The red herring: “technology is deflationary”

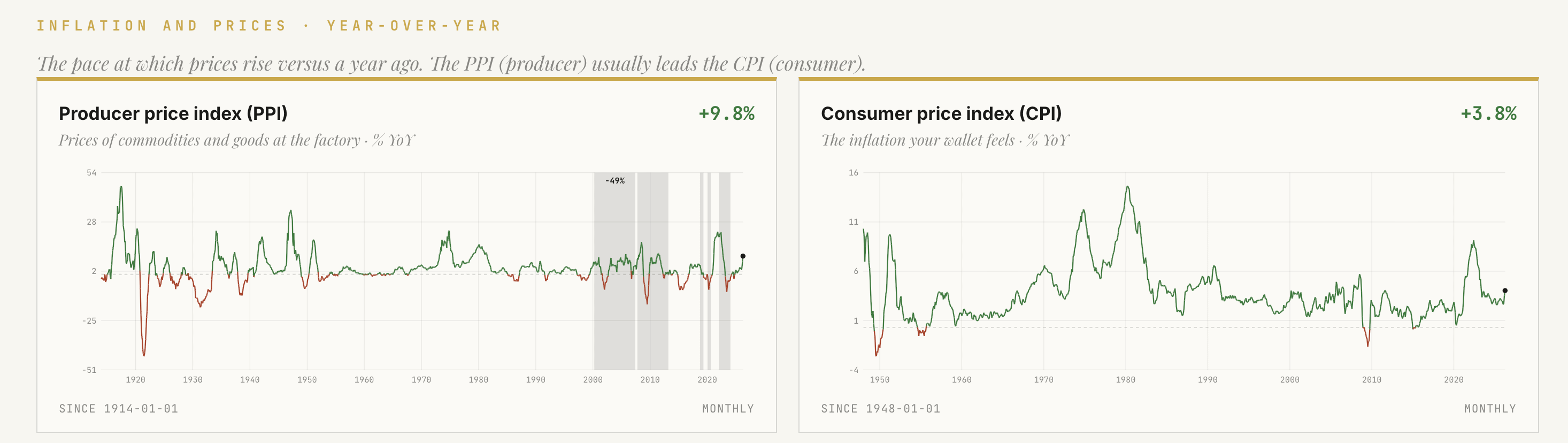

Now the misdirection everyone leans on. AI will crush prices. Ignore the inflation — the machines will eat it.

The data says otherwise. The Producer Price Index — prices at the factory gate, the goods that become everything else — is running +9.8% year over year. The Consumer Price Index, the inflation your wallet feels, is +3.8%. PPI leads CPI. The wholesale layer is already running near ten percent while the retail layer stays calm. That gap is not deflation. That gap is a pipeline.

So challenge the premise directly: technology does not automatically create deflation. It creates deflation only at one specific stage — and we are not in it.

Look at the first Cold War. In its early decades, the dominant designs of the microprocessor, of consumer electronics, of computing had not yet been settled. The deflationary, globalizing wave did not arrive with the technology. It arrived later — in the 1980s and 1990s — once standardization, scale, and supply-chain optimization had matured. Deflation is what the optimization phase produces.

We are not in the optimization phase. We are in the competition phase.

The motive: a war over dominant designs

Here is the motive that explains every clue at once. The world is now fighting to define the dominant designs of the next era — AI, robotics, compute, electricity, autonomous systems, strategic networks. Nothing is standardized. Everyone is building competing, redundant, sovereign versions of the same stack.

Why is fragmentation necessarily inflationary? Ronald Coase answered the question in 1937, long before anyone called it macro. Firms exist, he showed, because using the market is not free. Every transaction carries costs — searching for a counterparty, negotiating, writing the contract, enforcing it, guarding against betrayal. When those costs are low, you buy on the open market. When they are high, you make it yourself.

Globalization was the greatest transaction-cost compression in history. Stable rules, dollar settlement, enforceable cross-border contracts, low political risk — the whole planet became one cheap marketplace. So firms stopped making and started buying: anywhere, from anyone, at the lowest price. Value chains dis-integrated across forty countries because coordination had become nearly free. Disinflation was, in large part, transaction-cost deflation. The −0.26%/yr glide in rates during the Globalization era was its signature.

Cold War II runs the film backward. Oliver Williamson sharpened Coase with two variables that now haunt every boardroom: asset specificity and uncertainty. A chip fab, a rare-earth refinery, a sovereign AI cluster are extreme-specificity assets — priceless in the right hands, hostage in the wrong ones. And uncertainty — sanctions, export controls, a partner’s government weaponizing the relationship — has gone vertical. When specificity and uncertainty rise together, the theory gives exactly one answer: stop buying, start making. Internalize. Integrate. Build the redundancy.

So the world reshores, stockpiles, friend-shores, and builds parallel sovereign stacks. Each move is the rational response to higher transaction costs — and each is more expensive per unit, by design. The frictions globalization stripped out are being bolted back on: re-priced into PPI at +9.8%, and into the risk premium capital demands to fund any of it. This is the deep reason supply chains are now being rebuilt for redundancy instead of efficiency.

The conclusion is blunt: inflation here is not the printing press. It is the price of trust withdrawn from the system — and the structurally higher rate is simply that price, expressed as yield. You do not get the cheap, single-stack world that produced forty years of disinflation. You get its opposite.

And the scale is staggering. By the IEA’s reckoning, the five largest technology companies spent more than $400 billion in capital expenditure in 2025 — and that figure is set to rise around 75% in 2026. Data-center electricity demand is on track to roughly double to about 945 TWh by 2030 — close to the entire electricity consumption of Japan. In the United States, data-center power demand is projected to climb 130% by 2030; by the end of the decade, the country is set to burn more electricity running data centers than producing aluminum, steel, cement, and chemicals combined.

That is why compute is now a power problem before it is a chip problem. And it is why rates in this regime are not only pricing inflation. They are pricing geopolitical risk, supply-chain redundancy, energy competition, and strategic scarcity. The interest rate is the toll on a fragmenting world.

The long-term rate chart shows exactly this. The US 10-year has moved through distinct regimes: the Volcker shock added roughly +0.61%/yr, Globalization quietly bled it down at −0.26%/yr for a generation — and we have now flipped into “Rates 2.0,” rising at +0.62%/yr. That slope rhymes with Volcker, not with Globalization. The trend points to 6.5% by 2050.

For the monetarists: money is the unit, not the cause

A serious objection deserves a serious answer. Many readers hold that inflation is, in Friedman’s phrase, always and everywhere a monetary phenomenon — too much money chasing too few goods. If that is the whole truth, this entire structural story is noise, and only the money supply matters.

The objection is half right. The half it misses is the half that counts.

Start from the identity the monetarists themselves use: money times velocity equals prices times output — MV = PQ. Friedman’s dictum holds the real economy, velocity and productive efficiency, roughly constant, so prices track money. That assumption is the entire game. It is also exactly what Cold War II destroys.

A world rebuilding for redundancy instead of efficiency is a world deliberately lowering its own output per unit of input. Reshoring, dual supply chains, strategic stockpiles, energy competition, sovereign compute — each is a choice to spend more real resources to make the same goods. The denominator falls on purpose. So even with the money supply held perfectly still, prices rise — because the real cost of producing the basket has risen.

That is not a monetary impulse. It is a structural one.

Inflation may be a monetary phenomenon — but the floor beneath it is a real one. Money sets the number on the scale. The world decides the weight.

This is why no central bank can tighten its way back to the old regime. It can suppress the print, but not the floor — all it controls is who pays, growth or prices. The structurally higher rate is the toll on a fragmenting world, and the toll is real before it is ever monetary.

The reframe: higher rates are not a bear market

This is where the obvious suspect gets it wrong one final time. Rates are rising, so equities must fall. History says no.

Cold War I was a strong regime for equities — and a powerful one for commodities, industry, infrastructure, and energy. A world competing to build is a world spending capital at scale, and capital deployed becomes someone’s revenue. Rising rates and rising equities are co-symptoms of a buildout, not a contradiction.

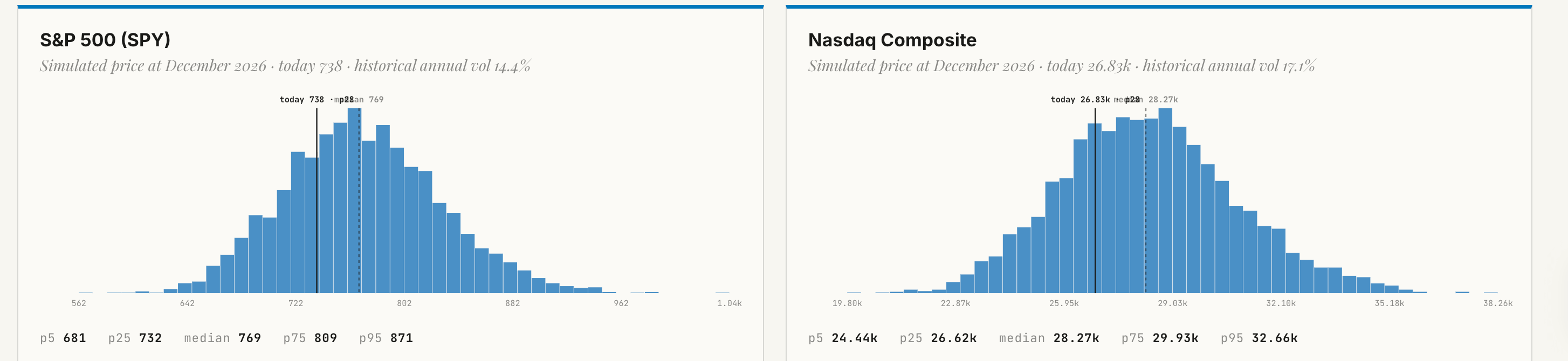

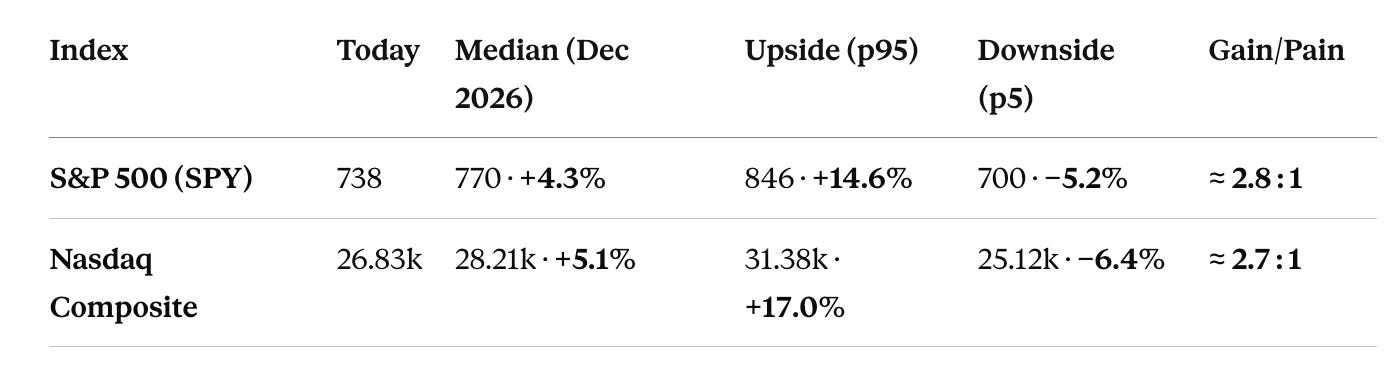

The probability distributions agree. Translated into year-end returns:

Read the ratio, not the headline. Both indices offer close to three units of upside for every unit of downside. The S&P carries the tighter ratio — a shallower left tail. The Nasdaq carries the bigger absolute upside, paid for with a deeper one. That is the higher-beta trade stated precisely: more upside per dollar, slightly more pain per dollar, the ratio roughly preserved.

And note how tight both distributions are: the 25th percentile of each index now sits at or above today’s price. Fewer than one in four simulated paths ends the year below spot. The market is not pricing a coin flip. It is pricing drift, with a floor.

So the verdict is not “crash.” It is violent rotation inside a rising tape.

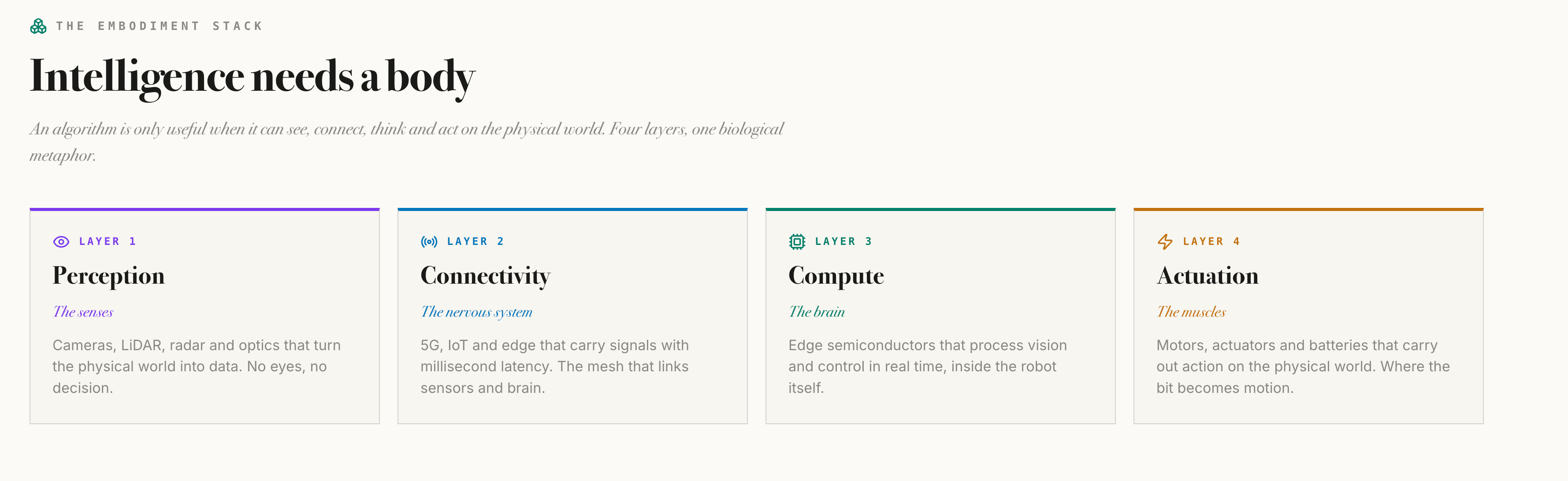

The clue everyone is missing: intelligence needs a body

Every eye is on compute. The entire market is pricing the brain — the accelerators, the training clusters, the silicon that thinks. That is exactly why the most important clue is being overlooked.

Intelligence, as biology actually built it, was never pure compute. Life’s strategy was never one giant cortex in a vat. It was embodiment and demography: millions of bodies, each carrying sensors and actuators, mapping reality by interacting with it. Intelligence scaled through population and contact with the physical world — not through raw thinking-power alone. The map of reality was drawn by an army of embodied agents, in parallel, over deep time.

Silicon intelligence today is a brain with no body. It can reason about the world; it cannot yet touch it, sense it, or act on it at scale. To cross that gap it needs precisely what biology needed — bodies, by the million, gathering real-world data and executing in physical space. That layer is robotics, and it is the single most underestimated bottleneck in the entire buildout. The market is fully priced for the cortex and barely priced for the limbs.

This reorders the hierarchy of scarcity. Compute is becoming abundant — capital is racing to manufacture it. Scarcity migrates to the next bottleneck, and the next bottleneck is the embodiment layer: the fleet, the sensors, the real-world data engine, the humanoid program.

Which forces the provocation this thesis cannot avoid. As of mid-2026, Nvidia is worth roughly $5 trillion — the most valuable company on earth, the brain of the buildout. Tesla is worth roughly $1.4 trillion — and is converting factories to build humanoid robots at scale, sitting on the largest real-world driving dataset in existence. If intelligence is valuable only once it can act on reality, then value migrates from the brain to the body as compute commoditizes.

Stated bluntly: on this thesis, Tesla could be worth more than Nvidia within three years. Not because the brain stops mattering — but because once compute is everywhere, the scarce thing becomes the body that turns intelligence into action. The market is staring at the semis. The next move is in the robots.

The verdict

The body looked like a death. The autopsy says relocation. Money is leaving the dollar-speculative canary (Bitcoin) and the energy-importing export economies (the yen, the won), and flowing into the bottlenecks of the next civilization-scale buildout:

Networks — the Nokia and Ericsson backbone, the Marvell silicon that moves data between accelerators.

Energy — GE Vernova turbines and grids, Bloom Energy fuel cells, because compute is a power problem first.

Embodiment — compute, electrification, and the robots that let intelligence touch the world.

This is the new Cold War: a competition for compute, robotics, electricity, AI infrastructure, and monetary power. Its signature will not be a clean trend. It will be turbulence, rotation, and dispersion — because no dominant design has yet been crowned.

So do not read the volatility as randomness, and do not read it as the end. Volatility is the market discovering the bottlenecks of the next civilization-scale buildout — and every spike is a clue about where the next decade gets built.

The detective’s last note: the crime was never a robbery. It was a relocation. Follow the money to the bottlenecks, and you find the trade.

Thanks for reading,

G

Guillermo Valencia A

Cofounder of MacroWise

Que buen artículo, todo en general me gustó mucho , pero dos cosas en especial me sorprendieron:

1. Tu posición con respecto a la inflación estructural en un mundo en donde no se premia la eficiencia sino la seguridad y redundancia (Q se ralentiza o cae y P sube en la ecuación que mencionas)

2. Tu intuición con respecto a la inteligencia y cómo la interacción con el mundo físico es aún más poderoso que la potencia en compute (long TSLA)

Gracias

eres un fenómeno Guillermo, que buena lectura