The Market Isn't Efficient, It's a Collective Intelligence Ecosystem

A vast network of agents—some vying for dominance, others pooling wisdom, a few sparking breakthroughs, and many echoing the crowd.

In 1970, Eugene Fama published a paper that changed finance forever. His Efficient Market Hypothesis (EMH) said markets are like perfect scorekeepers: every piece of information—earnings reports, news headlines, whispers of scandal—is instantly priced into stocks. Want to beat the market? Good luck. It’s like trying to outsmart a supercomputer with a pencil.

For decades, this idea ruled. It gave us index funds, the brainchild of John Bogle, who said, “Why pay a fund manager to chase returns when the market’s already figured it out?” Bogle’s logic was bulletproof: active managers rarely beat the S&P 500 after fees, so buy the index and chill. Investors listened. As of mid-2025, passive funds and ETFs manage over $27 trillion globally, with U.S. passive funds holding 47% of all fund assets, up from 15% in 2005. That’s a tidal wave of money betting on a flawed assumption.

But the market isn’t efficient. It’s a collective intelligence ecosystem, a vast network of agents—some vying for dominance, others pooling wisdom, a few sparking breakthroughs, and many echoing the crowd—where the whole emerges as a living, adaptive mind. EMH assumes we’re all rational, pricing assets against an objective reality. But reality is subjective, shaped by stories, beliefs, and hidden possibilities. Companies that optimize for profit are easy to value with spreadsheets. Those that harness collective insight or uncover game-changing secrets—like the internet’s network effects or electric cars’ potential—defy numbers until their impact reshapes the network. That’s why EMH needs a rethink. Let’s explore why, through stories and ideas that reveal markets as messier, more human, and more creative than EMH allows.

The 20% That Rule the Game

Imagine you’re at a party with 500 guests, but only 100 bring the vibe—music, drinks, the works. The rest just eat the snacks and leave. That’s the S&P 500. Data shows 20% of its companies drive about 80% of its returns. Think Apple, Nvidia, Amazon—these giants carry the index while hundreds of others tag along.

If markets were truly efficient, returns would spread evenly. Every stock would reflect its “fair” value, and no single group would dominate. But they don’t. Passive funds pour money into these winners, inflating their prices further. It’s a feedback loop: the big get bigger, and the market looks less like a level playing field and more like a winner-takes-all casino.

This isn’t new. In the 1920s, radio stocks like RCA soared as investors bet on the next big thing. Most crashed when the bubble popped. Today, AI stocks play a similar role. EMH says the market prices everything perfectly, but when a handful of stocks drive the bus, it’s hard to believe the passengers all pay the same fare.

Bubbles: When the Market Loses Its Mind

Didier Sornette, a physicist turned financial detective at ETH Zurich, studies market bubbles like a scientist tracking a collective frenzy. His work shows prices can spiral, climbing faster than fundamentals justify, then crashing spectacularly. He uses math—fancy stuff like Log-Periodic Power Law Singularity—to spot these surges before they break. In 2008, housing prices ballooned until they didn’t. In 2021, meme stocks like GameStop defied gravity, then fell back to earth.

Sornette’s point is simple: markets aren’t always rational. They’re driven by feedback loops, where optimism feeds more optimism until someone yells “fire!” and the herd stampedes. His models have predicted bubbles in real time, suggesting markets can be predictable in their madness. If EMH were right, bubbles wouldn’t exist—prices would never stray far from “fair.” But they do, because humans aren’t calculators. We’re storytellers, and sometimes we believe our own hype.

Andrew Lo’s Evolutionary Take

Andrew Lo, an MIT professor, sees markets as adaptive networks, not machines. In his book Adaptive Markets, he argues investors aren’t rational robots—they’re agents, evolving to survive. His Adaptive Markets Hypothesis (AMH) says efficiency isn’t fixed; it ebbs and flows. When the network is stable, prices settle. When a disruption hits—a crisis, a tech breakthrough—things get messy, and opportunities emerge.

Lo’s idea draws from biology. In a collective, the fittest agents thrive, but “fit” shifts with the environment. Markets are the same. In the 2008 crisis, banks failed because they couldn’t adapt to risks like mortgage-backed securities. Hedge funds that pivoted made billions. Lo’s AMH explains why 20% of stocks dominate: they’re best suited to today’s network—tech, innovation, scale. EMH assumes everyone plays the same game with the same rules. Lo says the game keeps changing, and so do the winners.

Peter Thiel’s Secrets: The Market’s Blind Spots

Peter Thiel, the billionaire behind PayPal and Palantir, offers a different lens. In Zero to One, he talks about “secrets”—truths about the world nobody else sees. Think of Google’s founders realizing search could organize the internet, or Elon Musk betting electric cars could be sexy. These aren’t just ideas; they’re game-changers, hidden until someone acts.

Thiel’s framework challenges EMH directly. If markets price everything perfectly, there’s no room for secrets. But secrets exist. In the early 2000s, Tesla was a long shot, dismissed by Detroit and Wall Street. Those who saw its potential—its secret—reaped massive rewards. Thiel says the biggest returns come from finding what others miss, not following the crowd. EMH assumes the crowd knows all. Thiel bets the crowd is often clueless.

This echoes Donald Rumsfeld’s “known unknowns” and “unknown unknowns.” Markets price the knowns—earnings, GDP, Fed policy. They struggle with the unknowns—disruptive tech, geopolitical shifts, or secrets waiting to be uncovered. Valuing a company like early Facebook, driven by network effects where value grows with its users, is guesswork until the network takes hold. Passive investing rides the knowns. The real money hides in the unknowns.

A New Game: The Prisoner’s Dilemma Reimagined

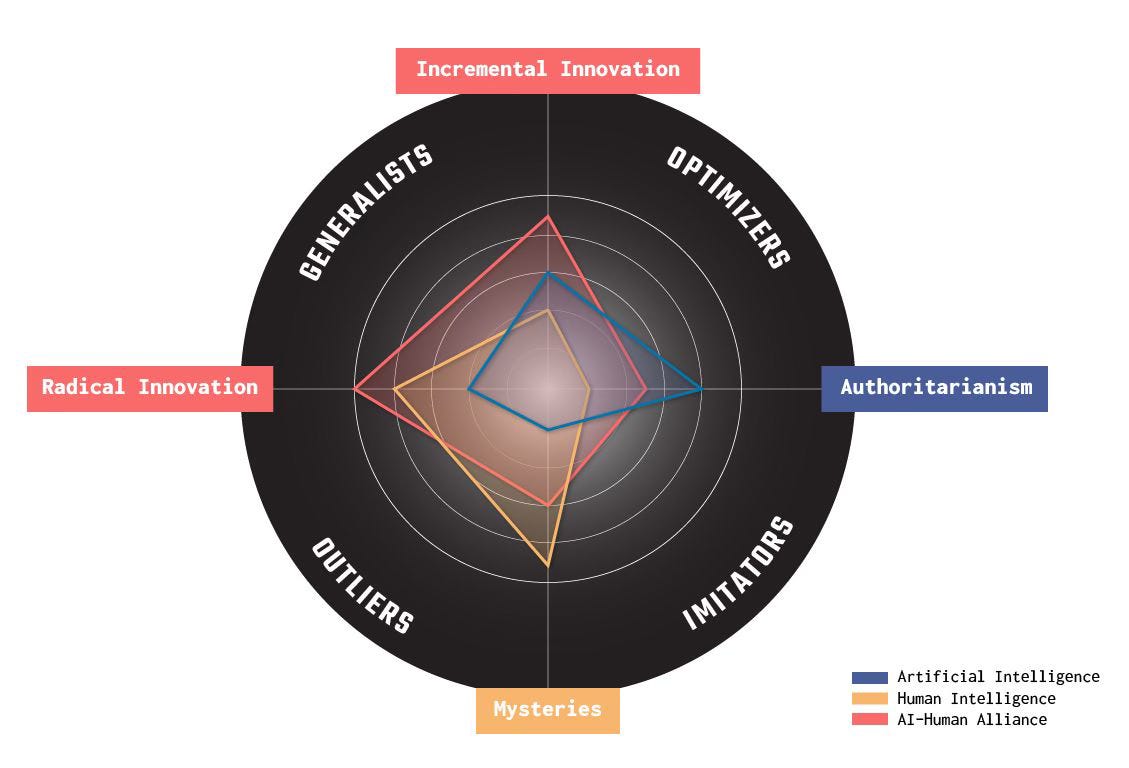

Let’s play a game. In the 1980s, Robert Axelrod ran tournaments based on the Prisoner’s Dilemma, where players choose to cooperate or compete. Cooperation often won, building trust over time. But markets aren’t just about trust—they’re about innovation, imitation, and survival. So let’s imagine a collective intelligence with four kinds of agents: those who compete, those who cooperate, those who create, and those who imitate.

Those who compete optimize, cutting costs and chasing efficiency—think hedge funds squeezing margins. It works until the network grows crowded, and growth stalls.

Those who cooperate pool ideas, blending strengths like open-source communities or industry partnerships, fostering steady progress but rarely breakthroughs.

Those who create seek secrets, risking failure for a chance at transformation—think the iPhone or SpaceX, rewriting the rules of their world.

Those who imitate copy the winners, piling into trends like tech stocks in 1999 or crypto in 2021, riding the wave until it breaks.

If everyone competes, the network thins—low margins, no progress. If everyone imitates, a bubble forms: huge gains, then a crash. Cooperation keeps the collective humming, but creation changes the landscape. The catch? Creation demands patience and risk. Few dare to try, but those who do—like Musk or Bezos—reshape reality.

This game reveals why EMH falls short. It assumes we’re all competing or imitating, pricing what’s known. But reality is a collective intelligence, a network of agents—some fighting for scraps, others blending ideas, a few sparking new paradigms. Fundamentals suit competitors, but cooperators and creators—whose value grows with networks or secrets—defy easy numbers until their impact unfolds. The market rewards those who cooperate or create, as bubbles prove and adaptation demands. Our power grows when we move from survival—competing and imitating—to creativity, where we redefine the world.

The Human Market

Here’s the lesson: markets aren’t efficient machines; they’re human stories. We’re not rational calculators—we’re dreamers, gamblers, and sometimes fools. EMH gave us a map, but it’s outdated. Bubbles, concentrated returns, and secrets show the terrain is wilder than Fama thought.

Passive investing is still a great tool. It’s cheap, reliable, and beats most pros. But it’s not the whole story. The market’s a collective intelligence, not a spreadsheet. To thrive, you need to adapt like Lo, hunt secrets like Thiel, and watch for bubbles like Sornette. Or, at least, know the game you’re playing.

Think of it like a road trip. EMH says the road is straight, the map is perfect, and you’ll arrive on time. Reality? The road twists, the map’s got gaps, and sometimes you find a shortcut nobody else saw. That’s where the adventure begins.

To dig deeper into these ideas, check out the works of the thinkers shaping this view:

Eugene Fama: The Foundations of Finance

John Bogle: The Little Book of Common Sense Investing

Didier Sornette: Why Stock Markets Crash

Andrew Lo: Adaptive Markets: Financial Evolution at the Speed of Thought

Peter Thiel: Zero to One: Notes on Startups, or How to Build the Future

Robert Axelrod: The Evolution of Cooperation

MacroWise Research

This graph illustrates how these strategies ebb and flow within the collective intelligence, with competition and imitation leading the charge, cooperation rising steadily, and creation sparking rare but transformative leaps—proof that our strength lies in embracing the unknown.

Thanks for reading,

Guillermo Valencia A

Cofounder of MacroWise

Barcelona , Spain

Excelente material ! Me parece que es una vacuna para evitar la enfermedad de la euforia colectiva en las inversiones !!