The Most Important Club: The USD

A new monetary standard is rising, but for now, expect Emerging Market currencies to remain weak in the shadow of a very strong USD.

The reserve currency is a common pool resource. The United States is the provider of this common pool resource necessary for international trade and finance. So basically, all countries without a reserve currency must hold their reserves in US Dollars.

Let’s think of this as a club where the US has a major part of the shares, but the world members have some shares proportional to their foreign reserves.

However, the monetary policy of the US optimizes their national interest, not the stability of a global currency. In times of crisis, the US will control inflation expectations, supporting economic growth and attempting to avoid high levels of unemployment.

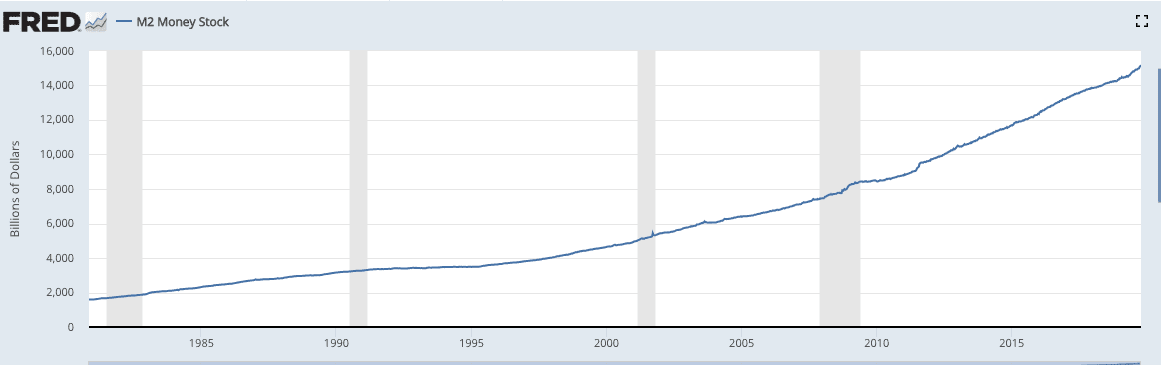

Money Supply M2. Source: St Louis Federal Reserve

We have seen such a crisis in 2008. The monetary base (M2) in the US has increased from $10 trillion at that time to nearly $16 trillion in 2019. So, the USD is being diluted for all of the members in the club. Suddenly, the representation in the global monetary system is lower because of US policy.

With the US stimulus policies aimed at COVID-19 and the quarantines impact, the size of this monetary easing could create a lot of instability in the international monetary system. The Fed is the major holder of the risk free asset, the US treasuries.

Source: yardemi.com

A way to have evidence of this is by measuring the price of Gold in emerging markets. One great example is Brazil since 2009.

Source: Tradingview.

Same works for the Indian Rupee since 2009

China

The most important disruption happening right now is in China, where Chinese reserves that peaked in 2014 at 36% proportionally, now only hold 23% of the US M2.

Source: St Louis Federal Reserve.

This is producing two outcomes in China: devaluation pressure and low economic growth. The quasi peg immediately reflects a decrease in reserves during a contraction of the monetary base, creating a contraction in the Chinese economy.

Saudi Arabia

One of the key factors for the USD as a reserve currency is the agreement with Saudi Arabia to support all oil transactions in USD. However, China is currently the biggest net oil importer in the world. That makes room to create a new deal where oil transactions could be settled in Yuan. US energy independence and the transition from Oil to Gas is moving the Saudi Strategic Interest towards China.

Saudi Arabia is another interesting country in all of this. The Saudi reserves in 2014 were greater than 6% proportionally of the US M2, but are now only 3.5%

Source: St Louis Federal Reserve

By Saudi Arabia having a peg, the contraction in reserves must be reflected in a very strong slowdown of their economy. That makes the case for reforms, the Saudi Aramco IPO and the longer-term Neom project and other long term investments.

Source: Financial Times.

Allowing a devaluation is not a good strategy for Saudi Arabia because they are basically a one product exporter. Oil devaluation would not create any improvement in their exports. In fact, it could make all the imports more expensive, increase inflation and perhaps even lead to more social turmoil throughout the region.

Another option is to redefine a peg against the Yuan or Gold.

Conclusion

Source: MacroTrends

The United States has used the USD in supporting their own national interests, which has in turn created instability across the global monetary system. The USD will continue as the best weapon in the United States’ fight to fend off the rise of China. However, this weaponization of the USD is creating social turmoil and geopolitical instability around the globe. As long as this trend continues, so too will devaluations across a multitude of emerging market currencies, but something has to change eventually.

A new monetary standard is rising, but for now, expect Emerging Market currencies to remain weak in the shadow of a very strong USD.

Guillermo Valencia A

Co-founder Macrowise

May 25 , 2020

Florianópolis, Brasil.