The Rolling Bubble

A macro detective story. Two charts that can’t share a decade, one weapon, and a market that has already told you where it’s going — if you read the evidence in the right order.

The crime scene

Every case starts with something that shouldn’t be possible. Mine starts with two charts that cannot belong to the same decade.

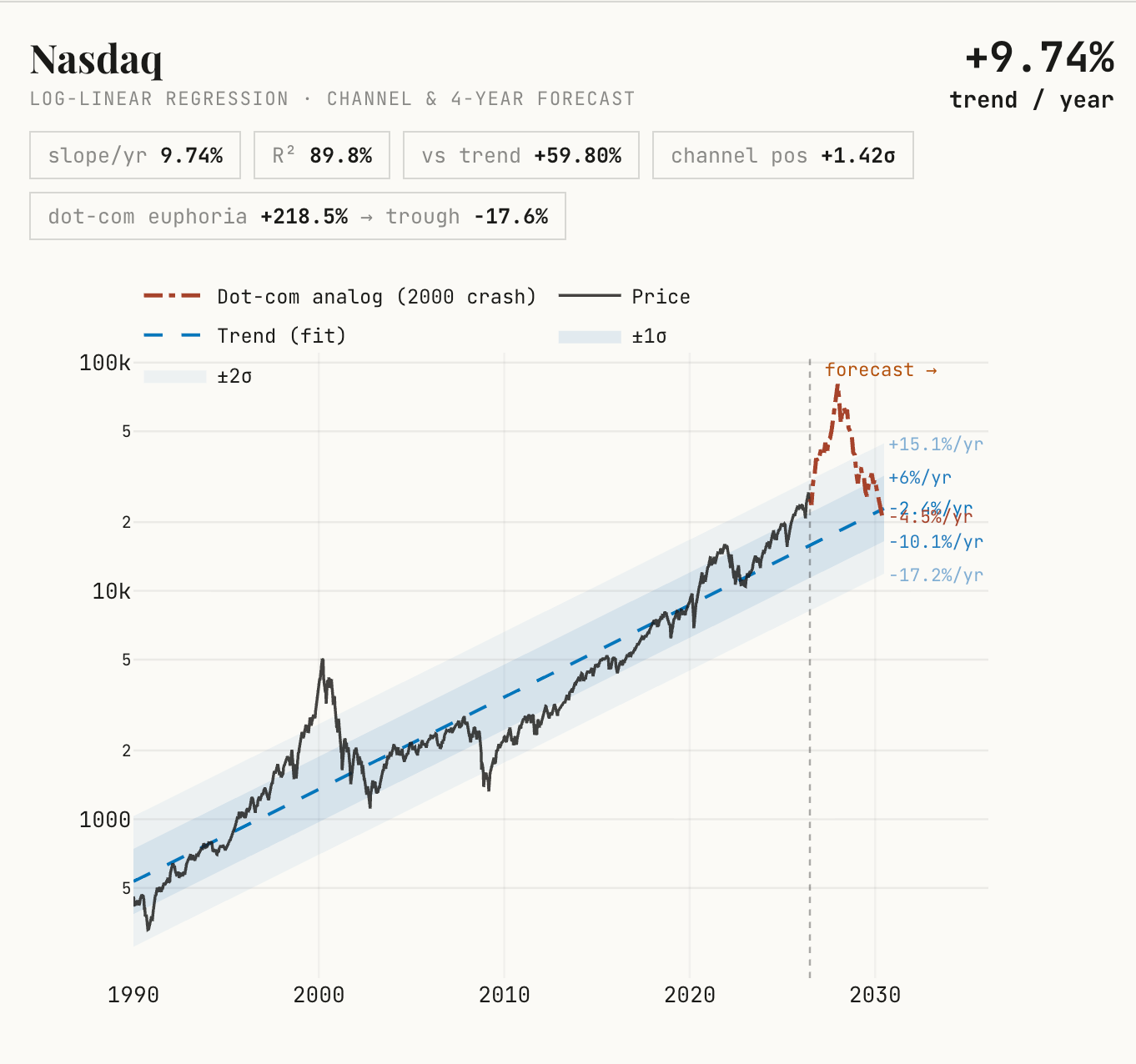

The first is the stock market trading like it is 1997. A trend that has compounded near ten percent a year for thirty-five years, price riding well above it, momentum in its bones — the kind of tape that, in the late nineties, did not roll over because it was expensive. It kept going because it was liquid.

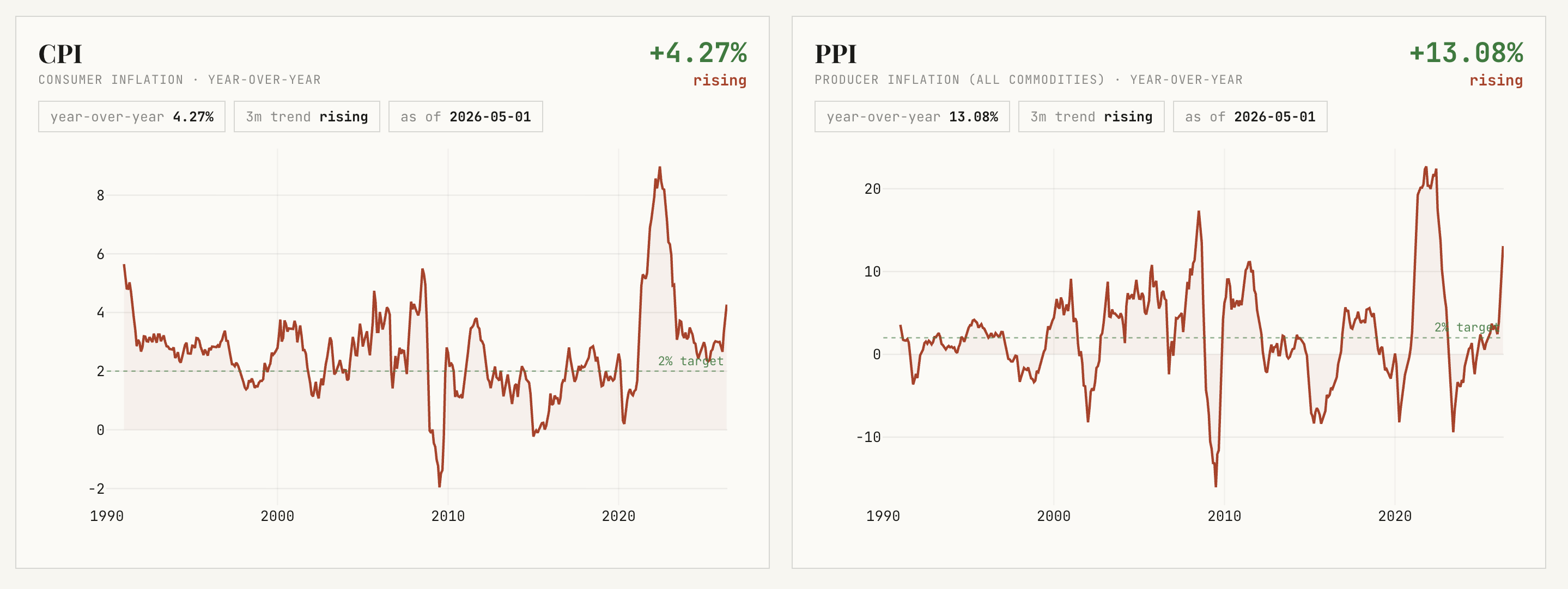

The second is inflation running like it is 2021. Producer prices up thirteen percent and still climbing. A cost-push impulse working its way up the supply chain before it has fully reached the till.

Two witnesses, two different decades, same room. The amateur picks the one he likes and calls it the truth. The detective assumes both are telling the truth and asks what single fact makes that possible.

I’ll tell you now where this ends, so you know what we’re driving toward. Somewhere in this market sit two companies running on the exact same fuel — one trading 357% above its long-run trend, the other 41% below its own. The crowd is convinced it knows which is the winner. By the end of this case, you’ll see it has them backwards. But to get there, we start with the bodies on the floor.

The weapon

Follow procedure: before motive, before suspects, find the weapon. The thing that made all of this happen.

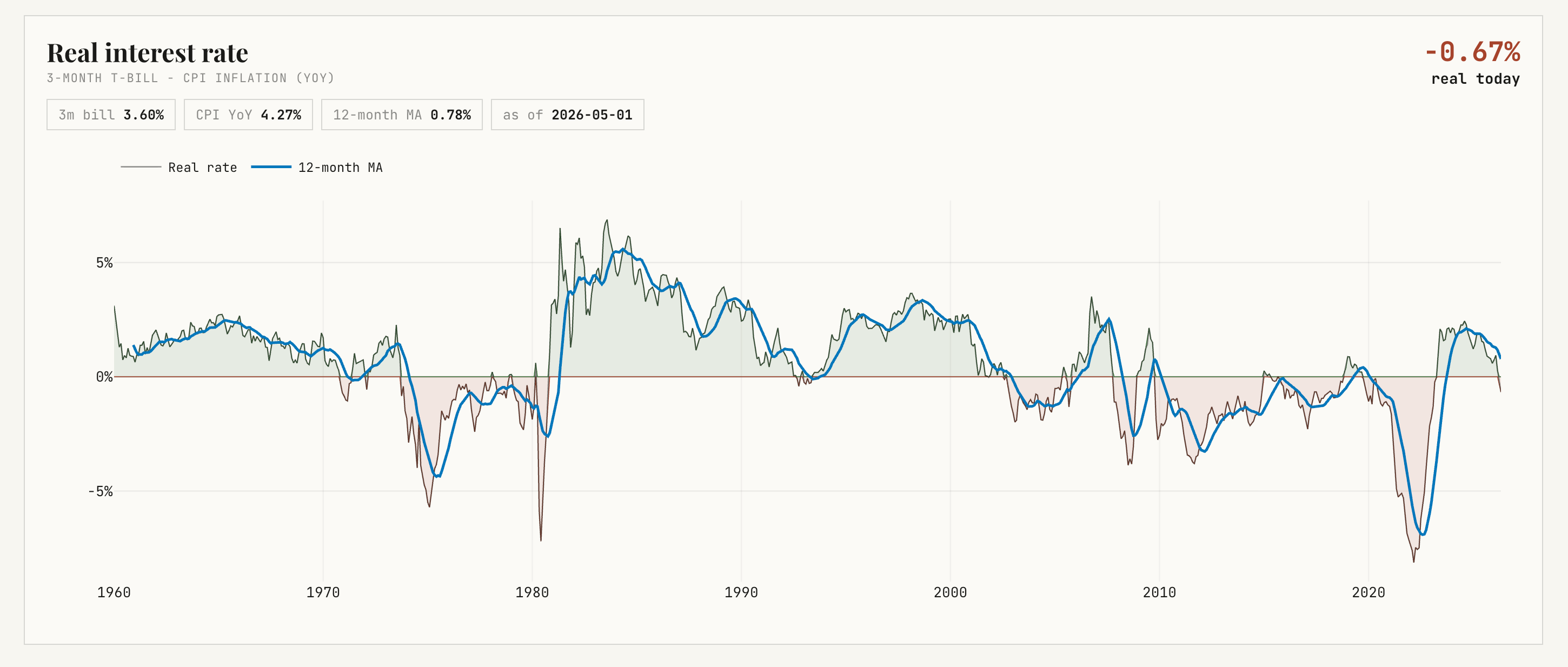

Here it is. The real interest rate is negative. The short bill pays less than inflation takes; money has been free, in real terms, for a year. This is the oldest mechanism in monetary economics. When the cost of money sits below the natural rate of return, the whole incentive structure of the economy reorganizes around owning real things and shorting cash. You do not get a contained recovery. You get a self-reinforcing expansion in everything nominal at once — asset prices and the price level together.

That is why the valuation bears keep getting carried out. As long as the real rate is negative, “isn’t this expensive?” is the wrong question. Expensive is a mean-reversion idea, and you do not get to use mean reversion in a regime whose defining feature is that the mean itself is being dragged higher by free money.

The weapon explains that there will be a crime. It does not tell you where the body is.

Following the money

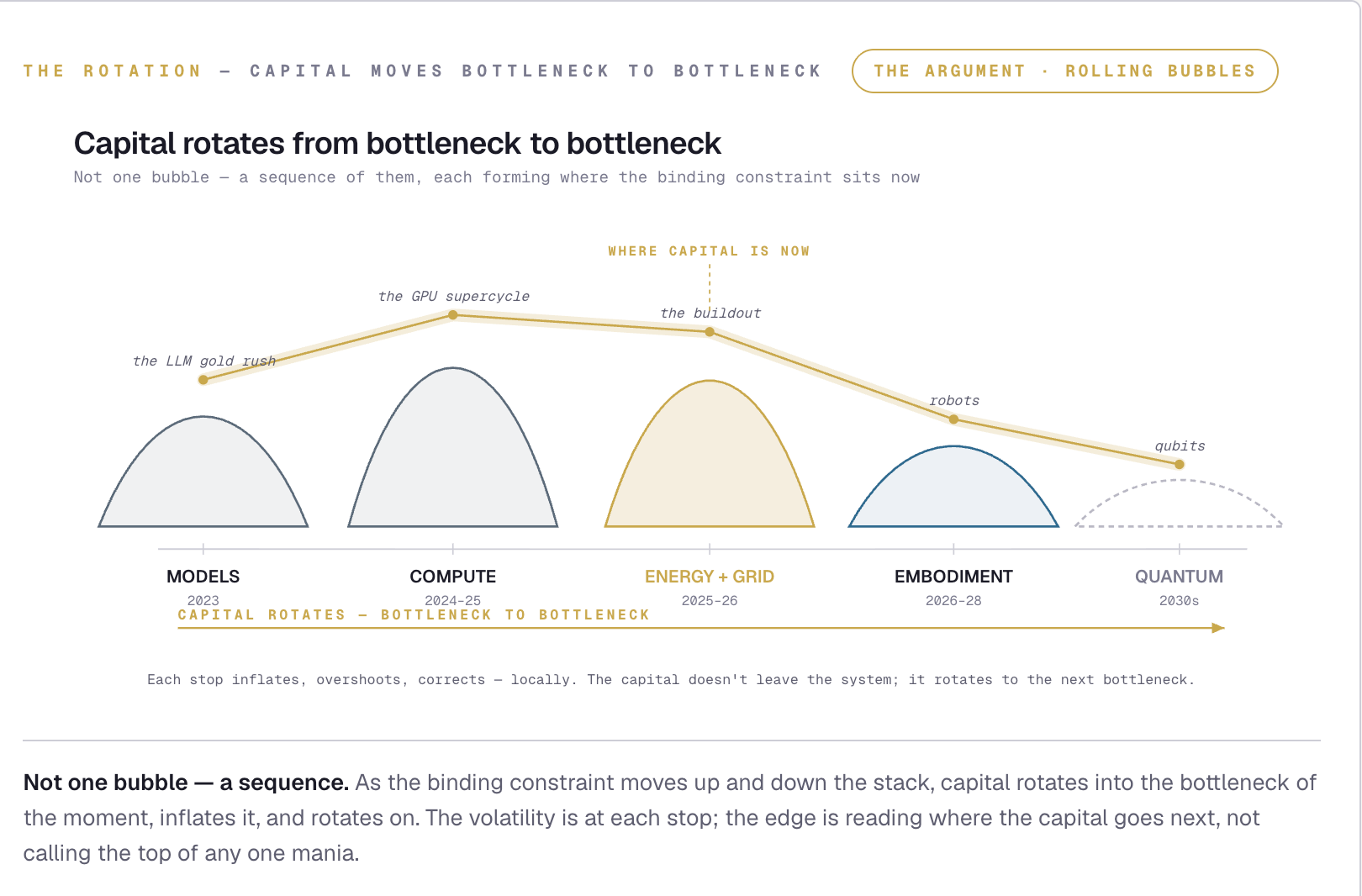

So follow the money. When a single constraint binds the whole economy and money is free, capital does not spread itself evenly. It floods the binding constraint, inflates it, overshoots, and — because the constraint is physical and eventually gets relieved — rotates to wherever the constraint has moved next. Not one bubble. A rolling bubble. A sequence of local manias, each forming where the bottleneck sits at that moment.

The trail is already legible, and your own diagram maps it. In 2023 the constraint was the models — the language-model gold rush, the most speculative, most 1997-flavored leg of the whole thing. By 2024 it had moved down to compute, and the mania rotated into the chip supercycle. By 2025 it moved again, to the place almost nobody had priced: energy and the grid — the buildout. That is where capital sits today. Two stops still lie ahead on the same arrow: embodiment, then quantum.

Each stop inflates, overshoots, and corrects — locally. The capital does not leave the system. It rotates to the next bottleneck. Which is why the edge is never calling the top of any one mania; it is reading where the capital goes next.

Read correctly, the technology stack is not a basket of themes to hold all at once. It is a clock. The binding constraint walks up and down the stack, and capital walks with it, one stop at a time. The rotation is not noise around the thesis. The rotation is the thesis.

And it closes the contradiction from the crime scene. The market looks like 1997 because the financial echo of the buildout still lives in the index. Inflation looks like 2021 because the physical reality of the buildout is hitting the cost side. Same event, read at two different floors.

The unreliable witness

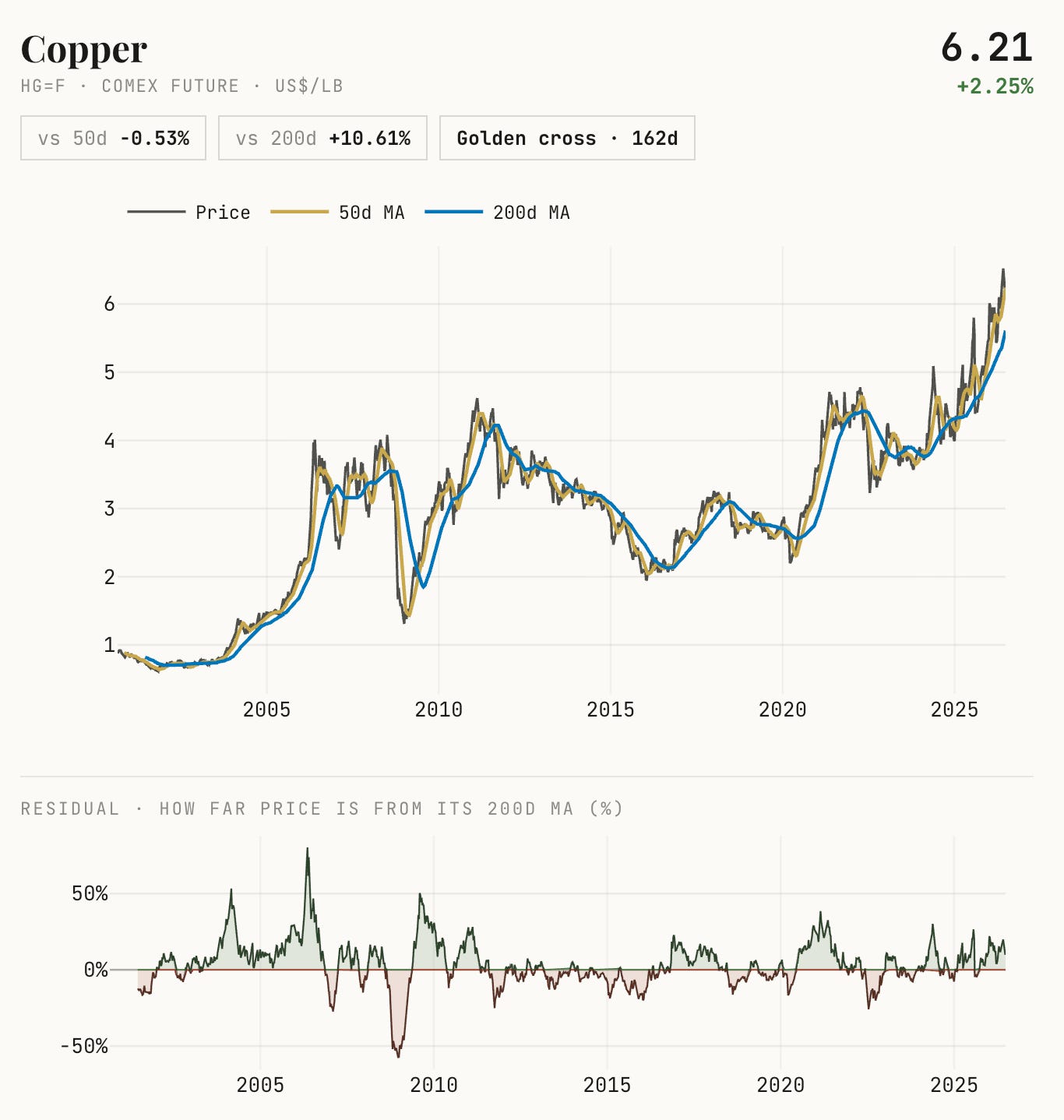

Every case has a witness everyone believes too easily. Here it is copper — and a good detective is most suspicious of the witness whose story is too convenient.

The convenient story goes: you cannot fake the demand for wire, so a rising copper price is physical proof the buildout has arrived. The trouble is that copper is one of the most financialized metals on earth, and much of its current premium is a financial artifact. American buyers have been hoarding metal ahead of an expected import tariff, swelling Western inventories. Several major mines were disrupted last year. And the consumer that actually sets the global price — China, half of all demand — is weak, not strong. On the desks that trade it, the market may even be in surplus, and at least one major bank argues the price has overshot fair value by a fifth.

So the witness is contaminated. If you are long copper as a pure AI trade, you are also unknowingly long a tariff decision and short Chinese consumption — which is not the bet you think you are making.

Move the claim off the price, where it is exposed, and onto the evidence that cannot be coached. A gigawatt of datacenter takes tens of thousands of tonnes of copper, and the grid to feed it takes more — but the binding constraint is not the metal in the abstract. It is the equipment. The largest technology companies are now outbidding utilities for transformers and switchgear, the copper-wound iron the grid itself runs on, and they are largely indifferent to what they pay. That is the un-fakeable fact: AI capital winning a bidding war against the power companies for the same hardware. You cannot finance your way around a transformer that takes two years to build.

So copper stays in the file as corroboration, not proof. As a read on the physical intensity of the buildout it is real — mine supply takes a decade to respond, ore grades have fallen for thirty years, and the demand drivers are arriving at once in a way no prior cycle saw. As a real-time receipt for where capital sits this quarter, the price is too compromised to lean on. The structural pull is the signal; the tariff trade and the Chinese air-pocket are the noise.

The witness who isn’t lying

When one witness is compromised, you look for the one with no incentive to flatter anybody. In this market, that is the bond market.

Long-term government bonds are falling and corporate credit is quietly weakening, even as stocks and commodities throw a party with volatility asleep. That divergence is the tell. A debt-financed, energy-hungry capex wave is exactly what keeps long rates elevated and producer prices running, and the bond market is pricing that regime while the stock market celebrates it. When the honest witness and the euphoric one disagree this cleanly, you do not split the difference. You note which one tends to be right.

And here a careful reader catches what looks like a contradiction, so let me cross-examine the witness before someone else does. The weapon was a negative real rate — free money, stimulus. Yet long bonds falling means long-term real rates are rising. Two real rates, pointing opposite ways. Which is it?

Both, and that is the whole regime. The front end — the short real rate — is negative, and that is the stimulus pulling capital into the rotation. The long end rising is the bond market pricing the inflation that the stimulus is causing. They are not in conflict. They are cause and consequence: the free money at the front lights the fire, and the long end smells the smoke. A debt-financed buildout that bids up transformers and copper is, mechanically, the thing that drags long real rates up while the short rate stays buried below inflation.

Which turns the apparent contradiction into the most important clue in the file — the exit clause, written in advance. The fire burns as long as the front end stays negative. The day the long end’s pull finally forces the front end positive — the day the short real rate has to climb above inflation to stop it — the stimulus reverses, and you are not in 2025 any more. You are in 2022, when a positive real rate took the whole nominal complex apart at once. That is not a risk hovering over the thesis. It is the thesis’s own off-switch, and the bond market is where it will trip first.

Where the suspect goes next

Here is the move that separates the detective from the crowd at the crime scene. The crowd investigates where the body is. The detective works out where the suspect goes next.

The crowd is staring at the leg that already happened. The discipline is to position for the world eighteen months out — to be early, and alone, on the next stop. And the next binding constraint is embodiment. Robots. The 2026-to-2028 stop on the rotation.

A fair question stops me here: why that window, and not 2030? Because the rotation is not arbitrary — each leg builds the precondition for the next. The embodiment leg cannot begin until three things cross a threshold at once, and the prior legs are what push them across it. A robot needs a brain cheap enough to put in every unit — that is the compute leg driving the cost of intelligence down. It needs power abundant enough to train and run that brain at scale — that is the energy leg, the one capital is funding right now. And it needs a machine actually designed to be mass-manufactured rather than hand-built — and the first such design is reaching a production line this year, not at the end of the decade. The robot leg fires when cheap intelligence, abundant power, and a manufacturable body arrive together. That convergence is dated to the next eighteen months by the legs that came before it, which is exactly why it is the next stop and not a distant one. Miss the convergence and the window slips; that is the risk. But the clock is the rotation’s own, not a number pulled from the air.

Which leaves the only question that matters in this whole case: who is the face of that leg?

The line-up

Every leg of this mania has had a face, and naming it is where most people get it wrong. So bring in the two suspects and put them side by side.

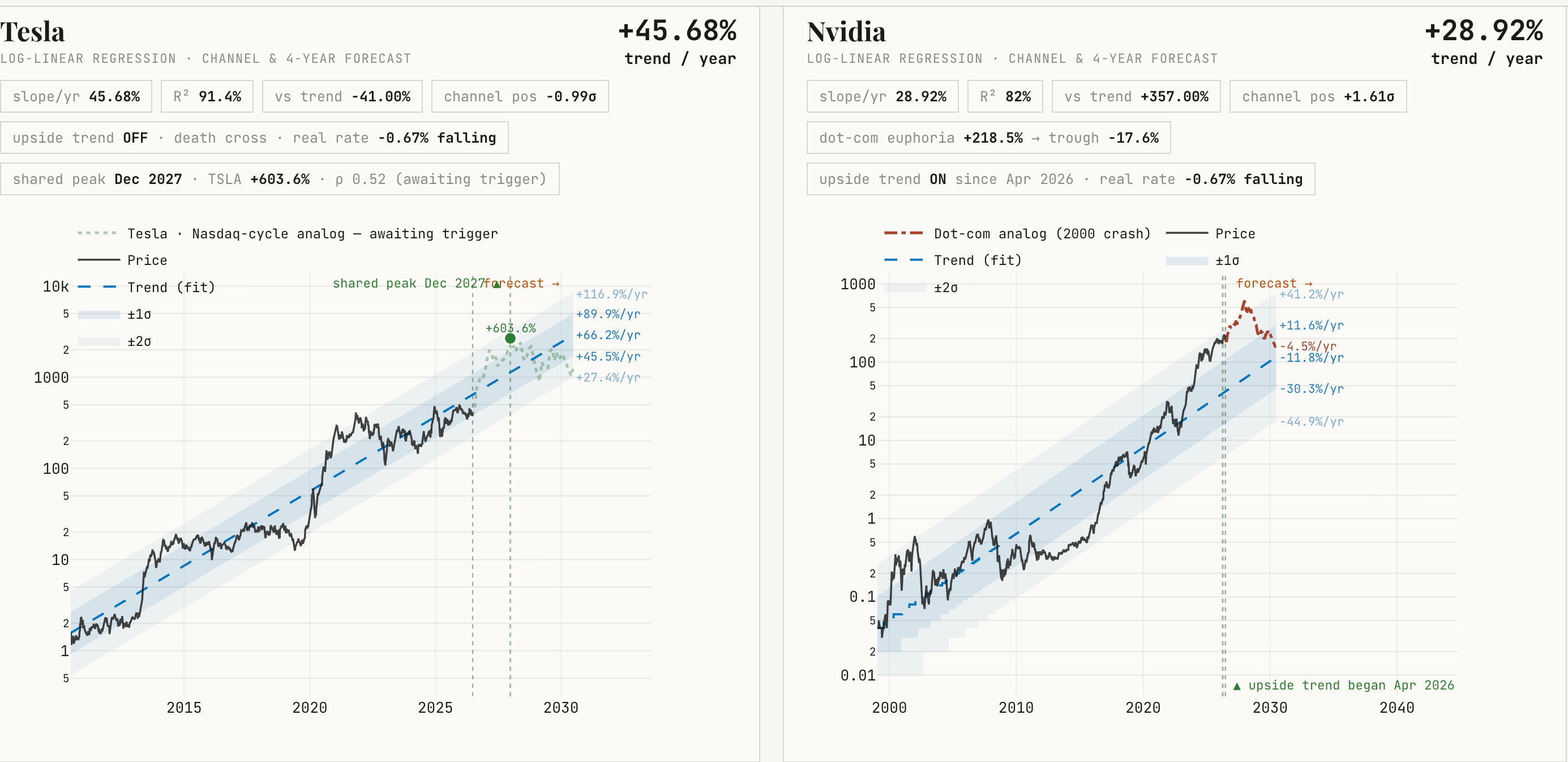

Look at what the line-up shows. Nvidia sits 357% above its own trend, at +1.61σ, upside trend on, with the dot-com crash pattern drawn across its forecast. That is the suspect who has already struck. Tesla sits 41% below its trend, at −0.99σ, upside trend off, marked plainly: awaiting trigger. That is the suspect who hasn’t moved yet.

And here is the detail that gives the case away. Tesla’s long-run trend compounds faster than Nvidia’s — roughly 46% a year against 29%. The faster-growing company is depressed below its line while the slower one is stretched to euphoria above its own. Both run on the identical fuel: a real rate of minus 0.67%, and falling. One tank is empty. One is full.

Now, the alibi the obvious suspect would offer — the one a good case has to break, not dodge. The face of the robot leg might simply be the face of the last one. Nvidia sold the brain to every model; it now intends to sell the brain to every robot, the same chips and software handed to every humanoid maker on earth, including Tesla’s rivals. If physical intelligence routes through one company’s stack the way digital intelligence did, the rotation does not crown a new king. It re-elects the old one. The defense rests on that.

Here is the crack in it. The compute leg had a single bottleneck — the chip — and therefore a single throne. The embodiment leg has two layers, and they are not the same throne: the brain, and the body built at scale. And the whole question reduces to one thing — whether intelligence, in robotics, stays scarce or becomes abundant.

If it stays scarce, the chip company wins again and Tesla is just one more body builder buying its silicon. But the brain is being sold to everyone, deliberately, as a platform. The moment the same intelligence is available to every manufacturer, intelligence stops being what separates the winner from the also-rans. It commoditizes. And when the scarce input commoditizes, the binding constraint does not vanish. It moves — to the body. To the problem of manufacturing a machine with thousands of moving parts, reliably, at a cost low enough to sell by the million, and to the real-world data required to make it actually work. That is not a silicon problem. It is a manufacturing problem and a data problem, and it happens to be the exact problem one company has spent fifteen years solving.

I should be honest about that company’s record, because the case is stronger for the honesty. Tesla has missed every production target it has set for its robot since 2021. It aimed for thousands of units last year and built a few hundred. A Chinese company most readers have never heard of already ships more humanoids than it does, and it has yet to show its machine doing sustained useful work without a human quietly steering it. The robot leg has not been won. Not by Tesla, not by anyone.

But the structural claim holds: value sat with the brain while the brain was scarce, and as the brain becomes abundant, value migrates to the body, the factory, and the data. That migration is the entire reason the last face of this cycle is a manufacturer and not a chipmaker. Tesla builds the whole machine and, more importantly, builds the factory that builds the machine — and its car fleet is already the largest real-world deployment of physical AI in existence, generating the one input even the chip company calls the hardest to get: data from the physical world.

The verdict — and the alibi that would clear him

A detective who explains every outcome has solved nothing. So here is the verdict with the alibi that would overturn it attached.

If, over the next eighteen months, Tesla’s robot begins doing sustained, autonomous, useful work while its cost per unit falls as volume climbs — then the body-at-scale is the moat, intelligence has commoditized as predicted, and Tesla is the face of the last leg. If instead every humanoid maker converges on the same outside brain and the only thing separating them is who gets the better chip allocation, then intelligence never commoditized, and the face of the last leg is the face of the first one wearing a different coat.

The catalyst is already on the calendar: pilot production this summer, the first real volume next year, the moment the company itself calls its “Model 3 moment.” It either arrives, or it slips again, as it has before. I am betting it arrives — and I have just told you exactly what would prove me wrong. That is the difference between a thesis and a hope. A hope explains every outcome. A thesis names the one that breaks it.

How to make the arrest

The verdict only matters if it tells you how to act, and how you act is most of the game. It is never whether you are right; it is how much you make when you are right and how little you lose when you are wrong.

So you stand where the capital is — the physical-economy beneficiaries of the buildout while copper corroborates the present leg — and you position into the next leg while its main suspect sits below trend, unloved, awaiting trigger. You stay light on long-term bonds, the wrong side of every leg of this. And you pre-wire the reversal, because conviction without an exit is not conviction, it is faith.

Three signals close the case, and you watch them daily. The real rate turns positive and stays there — that is the off-switch from the bond-market cross-examination, the 2022 trapdoor: it does not end one local mania, it switches off the weapon behind all of them. Credit breaks with conviction — the buildout has become a squeeze, and credit always knows before equities admit it. And copper goes vertical, then snaps — the current leg has blown off and the capital is rotating up the stack, most likely into the robots. The elegant part: the same metal that corroborates this leg is the alarm for its end.

The detective’s principle

We are not in a bubble waiting to pop. We are in a rolling bubble — a single mania, funded by free money, walking from models to compute to the grid and coiling for its next leg into robots. The line-up tells the rest: the suspect that already struck stands 357% above its trend with the crash pattern on its back; the suspect that hasn’t sits below its own line, awaiting trigger, running on a full tank of the same fuel.

I’ll admit the one thing that keeps me honest. The body-at-scale only inherits the throne if intelligence commoditizes, and I cannot prove it will — only argue it, and watch. There is a version of the next two years where the brain stays scarce, the chip company wins again, and the suspect I have pointed at turns out to have a perfect alibi. I have told you what would clear him, and I am watching for it as closely as I am watching for the trigger. A detective who isn’t a little troubled by his own case hasn’t looked hard enough at it.

But the crowd isn’t troubled by anything. It is still back at the crime scene, arguing about whether last year’s bubble was a bubble. That argument is already over. The next one — where the capital goes when it leaves the grid, and who owns the floor it lands on — has barely started, and almost no one is in the room yet. That is the only place the edge has ever been: not at the body, but one step ahead of where the suspect goes next.

The case isn’t closed. It has just moved to the next address. Follow the money. If it was worth your time, share it with someone who'd argue with it — those are the readers worth having.

Thanks,

G