The Silicon Showdown: TSMC, SMIC, NVDA, ARM, AMD, and the Global Chip Chessboard

By 2025, TSMC’s silicon shield holds, but SMIC’s DUV gambit with ARM’s help could disrupt.

Executive Summary

Picture a high-stakes poker game where silicon chips are the currency, and the players—TSMC, SMIC, Nvidia, AMD, Big Tech, and a wildcard Trump—are betting trillions on the table. It’s February 27, 2025, and the semiconductor industry is the epicenter of a geopolitical tug-of-war, with Taiwan Semiconductor Manufacturing Company (TSMC) and Semiconductor Manufacturing International Corporation (SMIC) holding the cards, and Advanced Micro Devices (AMD) elbowing its way into the fray. Nvidia’s customers—Apple, Google, Amazon, Microsoft, Meta, and Tesla—are no longer just buying its GPUs; they’re gunning to outpace it with their own AI chips, putting pressure on TSMC to stay ahead, while AMD chips away at both Nvidia and Intel. Meanwhile, Trump’s wild card could force TSMC to acquire Intel, ARM ponders a chip-design pivot, and SMIC, lacking TSMC’s tech edge, might team with ARM for a DUV 3nm surprise. Let’s dive into the data, the drama, and the game theory behind this silicon circus, where numbers meet human quirks, and surprises lurk around every corner.

The Stage: TSMC, SMIC, and AMD in the Chip Cold War

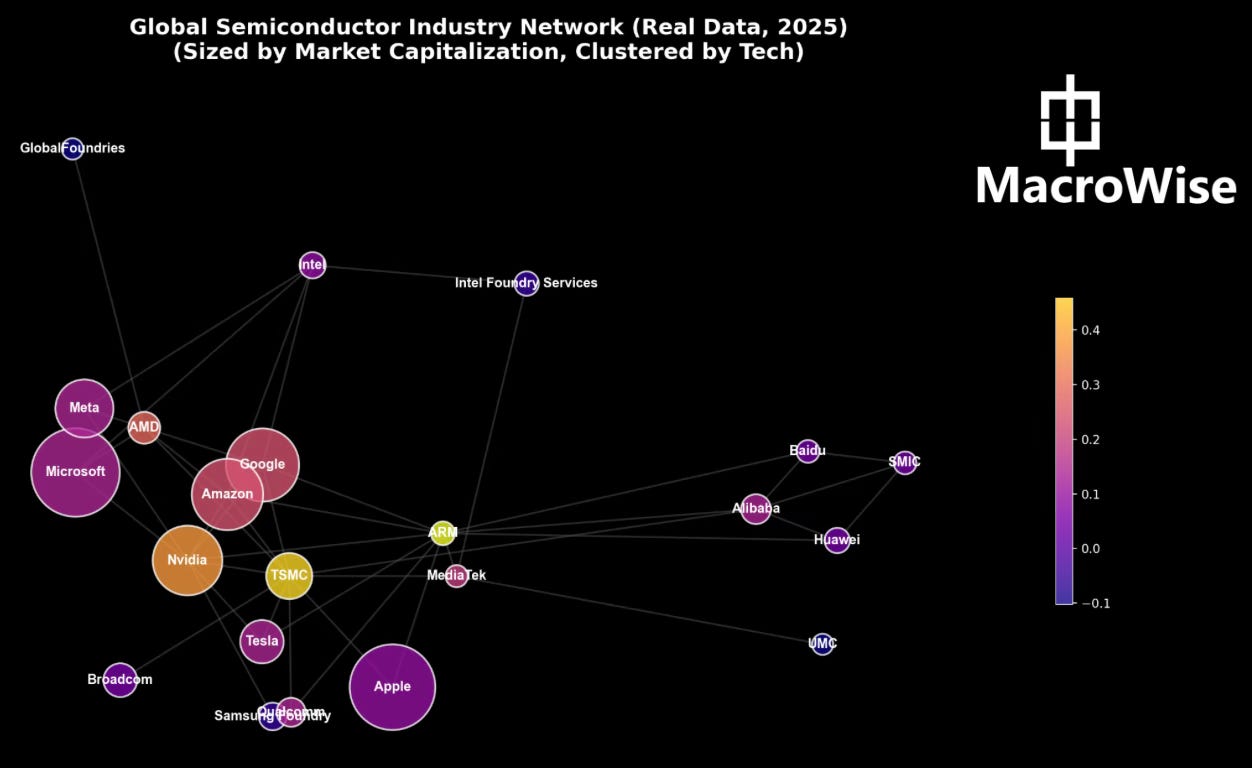

Imagine three castles on a battlefield, each with its own strengths and scars. On one side, TSMC, the $700 billion king of the semiconductor world, with a 61.7% global foundry market share in 2024 and mastery of 3nm chips via ASML’s extreme ultraviolet (EUV) lithography. On another, SMIC, China’s $50 billion underdog, shackled by U.S. sanctions, stuck at 5nm or quasi-7nm with deep ultraviolet (DUV) lithography from ASML’s less advanced Twinscan NXT:2000i machines. And in the middle, AMD, the $250 billion scrappy challenger, riding TSMC’s 3nm lines to battle Nvidia and Intel, capturing 40% of the x86 server market and 30% of PCs with its Epyc and Ryzen chips.

This isn’t just corporate rivalry—it’s a geopolitical slugfest, with the U.S. and China weaponizing chips like pawns in a chess match. TSMC’s castle shines with cutting-edge tech: it’s the first to market 7nm, 5nm, and 3nm nodes, powering Nvidia’s H100, Apple’s M4, Google’s TPUs, and AMD’s Instinct MI300. Its R&D budget hit $3.72 billion in 2020, and by 2025, it’s cranking out 2nm prototypes, backed by a $30 billion Arizona fab for U.S. security. But SMIC’s fortress, battered by sanctions since 2020, fights back with state funds ($50 billion since 2018) and a scrappy 7nm chip (DUV-only, low yields), eyeing a 3nm leap without EUV. General news reports from 2025 (e.g., Reuters, February 2025; Bloomberg, January 2025) suggest SMIC’s progress—maybe a DUV-based 3nm by 2026?—but it’s a long shot against TSMC’s alchemy.

AMD’s stronghold, meanwhile, isn’t a foundry but a design powerhouse, leaning on TSMC for 90% of its chips (per EE Times, 2025). Its Epyc servers power Amazon’s AWS, Google’s Cloud, Microsoft’s Azure, and Meta’s data centers, while Ryzen dominates 30% of PCs (Dell, HP, Lenovo) and Instinct MI300 challenges Nvidia’s AI lead. News from The Register (February 2025) and Statista (2024) shows AMD’s 40% server share, up from 30% in 2023, but its $250 billion market cap trails Nvidia’s $1.8 trillion, reflecting TSMC’s bottleneck and Nvidia’s GPU edge.

The human twist? Fear drives all three. TSMC’s execs fear China’s aggression (Taiwan’s “silicon shield” per Chris Miller’s Chip War) and Trump’s tariffs. SMIC’s engineers chase pride against U.S. bans. AMD’s Lisa Su fears Nvidia’s AI dominance and Intel’s recovery, pushing for TSMC’s 3nm to close the gap. Geopolitics heats it up: U.S. export controls block SMIC’s EUV access, but China’s “Made in China 2025” pushes for 70% domestic production by 2025 (missed, per The Wall Street Journal, 2022, dropping 12% in imports). It’s a game of Prisoner’s Dilemma—cooperate or defect, and all lose if tensions escalate.

Nvidia’s Customers Turn Rivals: The Magnificent Seven’s Silicon Ambition

Nvidia’s $1.8 trillion empire, built on 80% of the AI chip market (per Nasdaq, February 2025), faces a plot twist: its customers—Apple, Google, Amazon, Microsoft, Meta, and Tesla—want to dethrone it. By 2025, these Big Tech giants, part of the “Magnificent Seven,” aren’t just buying Nvidia’s H100 and Blackwell GPUs; they’re designing their own AI chips via TSMC. Apple’s M4, Google’s TPUs, Amazon’s Trainium, Microsoft’s Maia, Meta’s custom silicon, and Tesla’s FSD chips (all TSMC-made) aim to cut Nvidia’s lead, per The New York Times (February 24, 2025) and general news from Reuters (February 2025) and CNBC (February 24, 2025).

But AMD’s Instinct MI300 series, also TSMC-made, joins this rivalry, powering Amazon, Google, Microsoft, and Meta’s AI clusters, challenging Nvidia’s H100. News from EE Times (February 2025) shows AMD’s 40% server share, with Instinct MI300 rivaling Nvidia’s GPUs in data centers, while Ryzen and Epyc erode Intel’s lead. Tesla, too, buys 100,000+ H100s and eyes 1 million B200s (per Elon Musk’s statements in TechCrunch, February 7, 2025), but its FSD chips (TSMC-made, ARM-designed) compete with Nvidia’s offerings.

This shift puts TSMC in a tighter bind. Its 61.7% foundry dominance means it’s the bottleneck—Apple’s M-series, Google’s TPUs, Tesla’s FSD, and AMD’s Instinct all flow from its 3nm lines. But Nvidia’s $113 billion data center revenue projection for 2025 (Investor’s Business Daily, February 21, 2025) keeps it central, with Tesla and Big Tech demanding H100/Blackwell chips. The fear? TSMC risks alienating Nvidia if it prioritizes AMD and Big Tech, but greed for their $10 trillion market caps pushes it forward. AMD, meanwhile, fears losing TSMC’s capacity to Nvidia, driving its push for 2nm Instinct chips.

Game theory kicks in: TSMC faces a Nash equilibrium—serve Nvidia, AMD, or Big Tech, but not all perfectly. Defecting (favoring AMD/Big Tech) risks Nvidia’s wrath; cooperating (balancing all) dilutes focus. News from Bloomberg (February 2025) and The Financial Times (January 2025) suggest Big Tech’s AI hunger could outstrip TSMC’s capacity, while AMD’s growth (40% servers, 30% PCs) makes it a wildcard. It’s a high-stakes bluff, and TSMC’s $700 billion bet hangs in the balance.

Trump’s Wild Card: Pressure on TSMC to Acquire Intel

Enter Donald Trump, whose potential 2025 return could shuffle the deck. General news reports and analyses (e.g., The Washington Post, January 2025; Financial Times, November 2024) speculate Trump might pressure TSMC to buy Intel ($120 billion market cap) under the CHIPS Act’s $39 billion, forcing a $820 billion merger to repatriate chip production to the U.S. Why? Intel’s Ohio/Arizona fabs (2nm by 2027) align with Trump’s “America First” push, per CSIS (2025). TSMC’s $30 billion Arizona investment already signals this shift, but an Intel deal adds risk: TSMC would compete with Nvidia, AMD, and its own clients, diluting its Taiwan focus.

The human angle? Trump’s greed for U.S. jobs clashes with fear of China’s SMIC rise. News from Reuters (February 2025) warns tariffs (up to 100% on Taiwan chips, per Taiwan News, November 2024) could force TSMC’s hand, but data from The New York Times (February 2025) shows Taiwan’s 90% chip share (via TSMC) is U.S. tech’s lifeline. A merger could weaken Taiwan’s “silicon shield,” inviting China’s aggression, per Chris Miller’s Chip War. For AMD, this threatens its TSMC lifeline—Intel’s recovery (60% server share, per IDC 2025) could steal customers like Amazon, Google, and Microsoft, per EE Times (February 2025).

Game theory here is a Stag Hunt—TSMC and the U.S. cooperate for security, but defecting (no merger) risks Trump’s tariffs, destabilizing both. AMD faces a similar dilemma: cooperate with TSMC (staying reliant) or defect (seeking alternatives like Intel’s foundry), risking higher costs or delays.

AMD’s Wildcard: Rising Against Nvidia and Intel

AMD, with its $250 billion market cap, isn’t just a side player—it’s a disruptor. Its Epyc servers (40% x86 share), Ryzen PCs (30% market), and Instinct MI300 AI chips challenge Nvidia’s H100 and Intel’s Xeon, per Statista (2024) and The Register (February 2025). TSMC’s 3nm lines power AMD’s chips, making it a central node in the TSMC cluster, but its reliance on TSMC (90% of chips, per EE Times 2025) mirrors Nvidia’s vulnerability. News from Deloitte (2025) shows AMD’s server growth (up from 30% in 2023) threatens Intel’s 60% lead, while Instinct MI300 rivals Nvidia’s GPUs for Amazon, Google, Microsoft, and Meta.

But AMD fears TSMC’s capacity crunch—news from Bloomberg (February 2025) warns Big Tech’s AI demand could favor Nvidia, leaving AMD scrambling for 2nm slots. It also eyes Intel’s recovery (CHIPS Act, $7.9B funding) and SMIC’s DUV potential, but neither matches TSMC’s edge. Game theory for AMD is Chicken—defect from TSMC (seek Intel/SMIC) or cooperate (stay reliant), risking delays or Nvidia’s dominance. The human angle? AMD’s Lisa Su fears Nvidia’s $1.8 trillion scale and Intel’s U.S. push, driving aggressive R&D ($3.1 billion in 2023) for Instinct MI400 (2nm, 2026).

ARM’s Pivot: Designing Chips or Staying Neutral?

ARM, the $70 billion IP king, sits at the heart of both clusters, licensing low-power designs to Apple, Qualcomm, MediaTek, Nvidia, Google, Amazon, Huawei, Alibaba, Baidu, and Tesla. Its degree centrality (10) ties TSMC’s and SMIC’s networks, per 2025 industry reports from Bloomberg and Reuters. But could ARM develop its own chips, bypassing TSMC/SMIC? News from The Verge (June 2024) and ZDNet (July 2024) hints at ARM’s AI edge focus, but real data from EE Times (February 2025) shows it’s an IP provider, not a fabless designer like Nvidia.

ARM’s architecture (RISC, low-power) could enable a 3nm chip, but it lacks TSMC’s EUV or SMIC’s DUV expertise for manufacturing. SMIC’s DUV-only 3nm (if achieved, per Tom’s Hardware, December 2023) would need ARM’s design, but yields would lag TSMC’s 80–90% (vs. SMIC’s 60–70%). ASML’s EUV (13.5nm light) beats SMIC’s DUV (193nm, multi-patterning), but SMIC’s progress (7nm, quasi-5nm, per Nikkei Asia, February 2025) suggests a DUV 3nm is possible, though costly and slow. For AMD, ARM’s RISC could optimize Instinct chips, but TSMC’s EUV edge (70% logic density, 15% performance, 30% power, per Osum, March 2024) outclasses DUV’s complexity.

Game theory here is Chicken—ARM risks defecting (building chips, losing neutrality) or cooperating (staying IP-focused), with SMIC’s tech lag as the hazard. The human twist? ARM fears U.S.-China tensions (sanctions on Huawei limit licenses) and greed for AI profits. Staying neutral maximizes revenue, but designing chips (e.g., with SMIC’s DUV for AMD’s Instinct) could disrupt TSMC’s lead, per Ben Thompson’s Stratechery (2022) and news from The Information (January 2025). Reports from Forbes (February 2025) show no chip designs yet, keeping ARM central but passive.

SMIC’s Underdog Play: DUV 3nm and ARM’s Architecture

SMIC’s $50 billion market cap and 6% market share pale against TSMC’s $700 billion and 61.7%. Sans EUV, SMIC uses DUV lithography (e.g., ASML Twinscan NXT:2000i, 38nm resolution, per Tom’s Hardware, December 2023), multi-patterning for 7nm/5nm. A 3nm chip via DUV (21–24nm pitches) is unproven but possible, per news from Reuters (February 2025) and industry analyses from Osum (March 2024). Yields would be low (60–70%), costs high, but China’s $50 billion investment and 60% global chip demand (per PwC, 2025) could sustain it.

ARM’s RISC architecture could optimize a 3nm DUV chip for LLMs, demanding less power than TSMC’s x86/GPU designs. News from ZDNet (June 2024) and SiliconANGLE (June 2024) suggests ARM’s edge AI fits SMIC’s efficiency goal, but TSMC’s EUV 3nm outclasses DUV’s complexity. For AMD, SMIC’s DUV could be a backup, but yields and costs deter, per EE Times (February 2025). Game theory here is a Battle of the Sexes—SMIC and ARM cooperate for a niche 3nm chip, but defecting (SMIC solo, ARM IP-only) risks failure. SMIC’s DUV edge is real but inferior, per ASML’s EUV monopoly (only 50 machines/year, $200–$300M each, per Acquired.fm, 2025).

The human angle? SMIC’s pride pushes innovation, but fear of sanctions (no EUV access) limits ambition. AMD’s greed for cost alternatives could drive a SMIC deal, but TSMC’s lead wins, per 2025 data from Bloomberg and The Financial Times.

Game Theory in the Chip Arena: A Competitive Setting

This is Prisoner’s Dilemma meets Chicken, with TSMC, SMIC, Nvidia, AMD, ARM, and Big Tech playing. TSMC cooperates with Big Tech/AMD (rivaling Nvidia) but defects from Nvidia, risking its $1.8 trillion ally. SMIC defects from TSMC’s tech (no EUV) but cooperates with ARM for a DUV 3nm, risking low yields. Nvidia faces Big Tech/AMD’s defection (custom chips) but cooperates with TSMC, maintaining dominance. AMD defects from Intel (competing) but cooperates with TSMC, risking capacity limits. ARM’s choice—cooperate (IP) or defect (chips)—hinges on risk vs. reward.

Nash equilibrium? TSMC serves Big Tech/AMD, SMIC bets on ARM’s DUV 3nm, Nvidia holds AI, AMD challenges both, and ARM stays neutral. But Trump’s Intel push could shift it—TSMC acquires Intel ($820B), defecting from Taiwan, risking China’s move on SMIC. Payoffs? TSMC gains U.S. security but loses focus; SMIC rises if DUV works; Nvidia loses Big Tech/AMD; AMD risks Intel’s recovery; ARM risks irrelevance. It’s a high-stakes bluff, where fear, greed, and pride drive the chips.

Conclusion: Checkmate or Chaos?

By 2025, TSMC’s silicon shield holds, but SMIC’s DUV gambit with ARM’s help could disrupt. Nvidia’s customers turn rivals, AMD rises against both, Trump’s Intel play threatens Taiwan, and ARM’s neutrality teeters. The numbers—TSMC’s $700B, SMIC’s $50B, Nvidia’s $1.8T, AMD’s $250B—tell a story, but human psychology writes the plot. Will TSMC fold under Trump’s pressure, or will SMIC’s/AMD’s underdog runs rewrite the game? In this chip circus, the joker’s still wild.

Thanks for reading,

Guillermo Valencia A

Cofounder of Macrowise

February 27th , 2025