Zombies to Rockstars

Three companies the market left for dead — GE, Intel, Nokia — are quietly running the next decade. Here’s the trade behind the trade.

There’s a word investment bankers use, quietly, about companies that aren’t really dead but aren’t really alive either.

Zombie.

The stock chart goes flat. The CEO gets fired. The annual report becomes an apology letter. Analysts stop covering it. The company keeps walking around — companies have an annoying habit of doing that — but the market has moved on.

Three of the most important industrial companies in the West were zombies in the last decade.

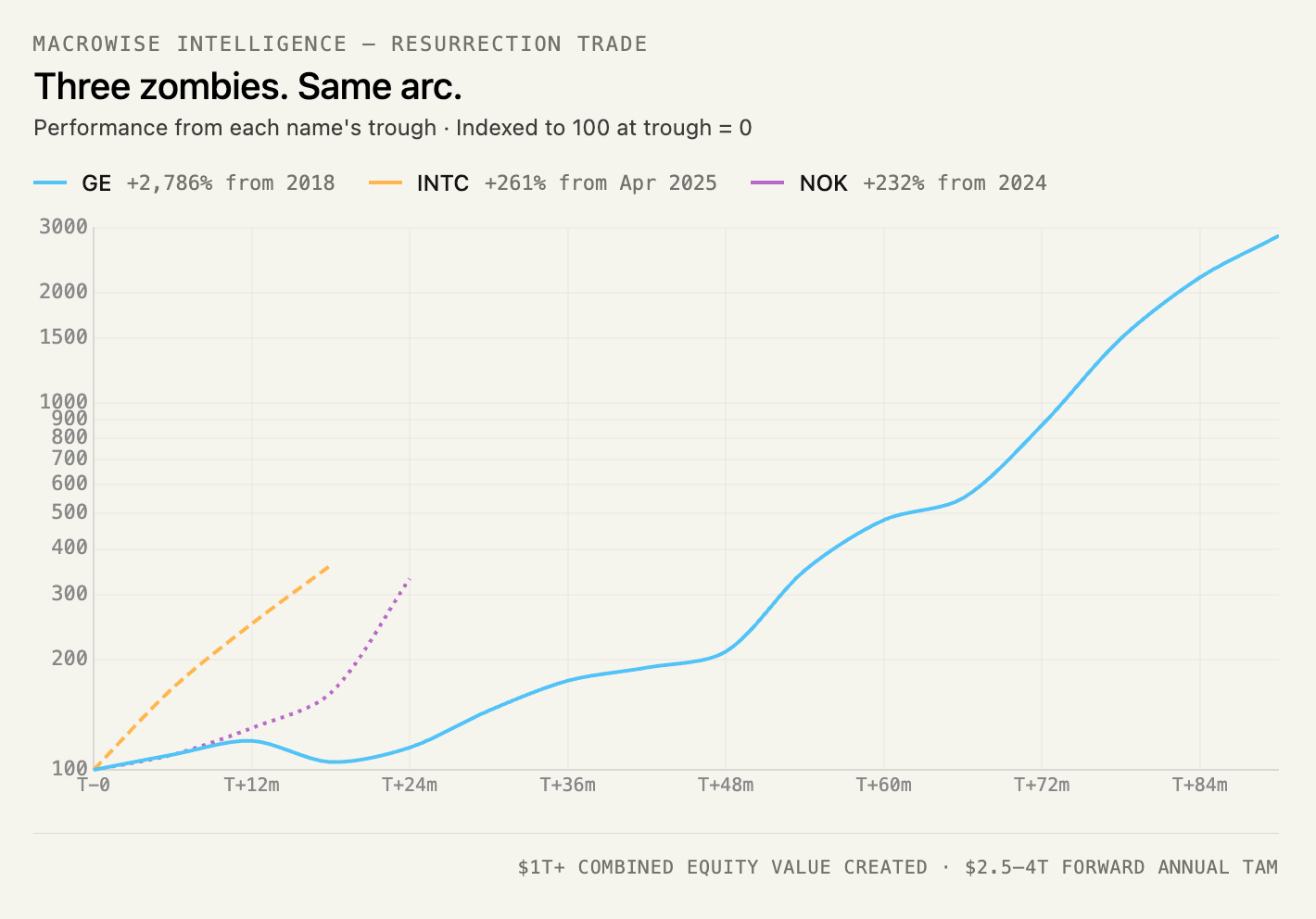

GE. Down 80% from its peak. Kicked out of the Dow in 2018 after 110 years. $140 billion in debt against a market cap that shrank below it.

Intel. Below $18 a share in early 2025. Missed mobile. Missed AI. Missed its own manufacturing roadmap two nodes in a row. Rumors that TSMC would buy parts of it.

Nokia. Sold its phone business to Microsoft in 2014 for $7.2 billion — pennies on the dollar. The brand vanished so completely that most people under 25 don’t know what it does.

This post is about how all three came back.

Not the half-comeback. Not the dead-cat bounce. The full reversal — the kind that makes people who sold at the bottom go quiet at dinner parties.

By spring 2026, the three of them have created roughly $1 trillion in incremental equity value. Combined forward TAM: $2.5–4 trillion annually by 2030.

The trade isn’t AI. It isn’t China. It’s something simpler. And it’s not over.

The Same Disease

Each was killed by the same thing: too diversified, in a world that stopped rewarding diversification.

GE made jet engines, washing machines, TV shows, insurance, and lightbulbs. The conglomerate model worked for 30 years. Then capital got cheap, the managers got worse, and the market started paying less for the whole than for the sum of its parts.

The technical term: conglomerate discount.

The plain translation: we don’t believe you anymore.

Intel made CPUs, modems, memory, GPUs, self-driving platforms, software, and ran its own foundry. It tried to do everything in semiconductors.

It lost two wars at the same time.

The factory war to TSMC — a Taiwanese company that did exactly one thing. Manufacture chips for other people’s designs. Apple fired Intel and switched to TSMC in 2020. Then everyone else did.

The architecture war to NVIDIA — a company that, 20 years earlier, made graphics cards for video games. While Intel doubled down on x86 CPUs, NVIDIA quietly built CUDA, the software layer that made GPUs the only chip that mattered for AI. By 2023, every dollar of AI capex on Earth was flowing to NVIDIA. Not Intel.

Intel wasn’t just losing manufacturing to Taiwan. It was losing the paradigm to Santa Clara.

The cruel part: NVIDIA had been a tiny gaming company in 2010 when Intel was the most powerful name in technology. By 2024, NVIDIA’s market cap was 30x Intel’s.

The student had eaten the teacher.

Nokia made phones, network gear, tablets, operating systems, map software. When the iPhone launched in 2007, Nokia had four operating systems running in parallel and couldn’t pick one.

Three companies. Three industries. Same disease.

The Same Cure

Break it apart. Pick the one thing you’re still better at than anyone else. Become great at that one thing.

Then wait.

The waiting is the part nobody writes about. The waiting is what ends the careers of executives who try this and don’t get lucky with the macro.

But when the macro turns — and the macro always turns — you don’t have to pivot. You just have to exist.

GE: The Template

In 2018, GE hired Larry Culp. First outsider CEO in the company’s 126-year history.

He came from Danaher. He believed in lean manufacturing. He was the opposite of Jack Welch.

Over six years, Culp paid down $100 billion of debt. Sold the lighting business. Sold the locomotive business. Sold pieces of GE Capital.

Then in November 2021, he announced what would have been heresy under Welch: GE would be broken into three.

GE HealthCare spun off January 2023.

GE Vernova (energy, turbines) spun off April 2024.

What remained — jet engines — became GE Aerospace.

The math today is almost embarrassing.

Combined market cap of the three pieces: ~$700 billion.

GE Aerospace alone: $330B. GE Vernova: $263B. GE HealthCare: ~$40B.

The old GE conglomerate at its 2018 trough: $80 billion.

Same buildings. Same people. Worth nearly 9x more broken apart.

GE Aerospace stock: nearly tripled since the breakup. GE Vernova: up 198% in the past year. Backlog: $190B at GE Aerospace, $150B at Vernova — including $2.4B of data center electrification orders booked in a single quarter. A category that didn’t exist in 2018.

The Wall Street nickname now: “the GE renaissance.”

Nobody calls it a zombie anymore.

Intel: The State Rescue

GE was sick but solvent. Intel, by 2025, was a national emergency.

America had exactly one company that could manufacture leading-edge chips on American soil. Apple’s chips were made in Taiwan. NVIDIA’s chips were made in Taiwan. The Pentagon’s chips, at the most advanced node, were made in Taiwan.

Taiwan is 110 miles from a country that has spent 70 years promising to take it back.

The military planners in Washington called it “the Taiwan question.” They preferred not to write down the answer.

On August 22, 2025, Washington did something it hadn’t done in a generation outside of a financial crisis.

It bought 10% of Intel.

The mechanics:

Intel was owed $5.7B in unpaid CHIPS Act grants.

Plus $3.2B from a defense program called Secure Enclave.

Total: $8.9B.

Converted into 433.3M shares at $20.47.

Stake: 9.9% non-voting.

Plus a five-year warrant for an additional 5%, exercisable only if Intel ever tried to sell its factories.

That warrant is a poison pill. It says, in legal English: the manufacturing arm is not for sale.

A month later, NVIDIA invested $5B at $23.28.

Read that sentence again.

The company that killed Intel — that took the architecture, that ate the AI capex, that was 30x Intel’s market cap by 2024 — was now writing Intel a $5 billion check at a slight discount to market.

Why?

Because even NVIDIA can’t afford for Intel to die. NVIDIA still needs CPUs to pair with its GPUs in every server rack on Earth. NVIDIA still buys from TSMC and is one missile strike away from a 90% revenue loss. And NVIDIA — for all its trillion-dollar swagger — depends on x86 servers, x86 hyperscaler infrastructure, and a U.S. government that is now Intel’s largest shareholder.

The student had eaten the teacher. Now the student was paying to keep the teacher on life support.

SoftBank put in $2B. In April 2026, Intel joined Elon Musk’s Terafab project in Texas — the chip-manufacturing venture between Tesla, SpaceX, and xAI targeting one terawatt of compute per year.

The U.S. government, NVIDIA, SoftBank, and the Musk industrial empire are now all on Intel’s cap table or in its supply chain.

Stock: $18 → $65 in 14 months.

A 261% rally that wasn’t a recovery. It was a reclassification.

Intel isn’t being valued as a chip company anymore.

It’s being valued as infrastructure.

Nokia: The Slow Phoenix

This is the strangest of the three.

Most people know the story that ends in 2014: Microsoft buys the phones, the Finns lose, the brand fades into a memory of indestructible Nokia 3310 handsets and a game called Snake.

What most people don’t know is what Nokia spent the next decade doing.

Buying things.

In 2016, Nokia acquired Alcatel-Lucent for $15.6 billion.

Inside Alcatel-Lucent — almost as a footnote — was Bell Labs.

Pause on this.

Bell Labs is where the transistor was invented in 1947. Where the laser was invented in 1958. Where Unix was written in 1969. Nine Nobel Prizes.

By 2016, all of it was Finnish.

Nobody noticed. Bell Labs was a rounding error inside a struggling European telecom company. Nokia stock traded between $3 and $5 for nine years.

Then on October 28, 2025, Jensen Huang stood on a stage in Washington and announced NVIDIA was investing $1 billion in Nokia at $6.01 a share.

The deal: NVIDIA’s GPUs would be embedded directly into the radios on cell towers. Every base station becomes a small AI data center.

Market size: $200 billion cumulative by 2030, per Omdia.

Nokia’s CEO, Justin Hotard, took the job in 2025. He came from Intel. T-Mobile signed on as the first U.S. customer.

Six months later, Nokia stock tripled.

Q1 2026 earnings raised the AI-and-cloud growth forecast from 16% to 27% CAGR. JPMorgan raised its price target from €6.90 to €12. Morgan Stanley from €8.50 to €11. The stock hit a 16-year high.

The phone-maker that failed had become the company that builds the network the AI runs on.

It didn’t pivot. It just waited.

The Pattern

Same shape, three times.

Each company was punished for being a generalist in an era that demanded specialists.

Each one shrank — sometimes voluntarily, sometimes not — to a single core competency.

Each waited.

And when the macro turned in their favor, none of them had to pivot. They just had to be there.

GE Aerospace didn’t invent the post-COVID aerospace supercycle. It just happened to be the only Western company that could service half the world’s narrow-body jet engines when air travel came back.

Intel didn’t invent sovereign semiconductor policy. It just happened to be the only American company with leading-edge fabs when Washington decided this mattered.

Nokia didn’t invent AI-native networks. It just happened to own Bell Labs and a global telecom-equipment business when NVIDIA needed a partner to put GPUs on cell towers.

The thing they had in common wasn’t innovation.

It was survival.

The Numbers

Three opportunity pools. All large. All early.

1. The aerospace supercycle.

70,000 GE/CFM commercial engines installed worldwide. Each one a multi-decade annuity. Boeing and Airbus delivery delays are forcing airlines to fly older planes longer — which means more service revenue per engine.

Global commercial aviation services TAM: $200B+ annually by 2030. GE share at the narrow-body services layer: ~50%.

2. Sovereign semiconductors.

Western capacity expansion needed to meaningfully de-risk from Taiwan: ~$1.5–2 trillion in cumulative fab capex over the next decade.

Intel is one of two non-Taiwanese companies with the technology to compete at the leading edge. Government willingness-to-pay is now functionally unbounded.

Sovereign-AI chip demand alone (defense, federal cloud, “never leaves U.S. soil”): $50–100B annually by the late 2020s.

3. AI-native networks.

ChatGPT users went from 205M monthly actives in August 2024 to 557M a year later. Half use it on mobile.

AI-RAN equipment market: $200B cumulative by 2030, growing at 63.5% CAGR. Total telecom capex by 2030: $545B annually.

Nokia and Ericsson are the only two Western pure-plays. Huawei is locked out of half the world.

The Entry Points

Spring 2026.

GE Aerospace at $286: 39x current earnings. Rich on current EPS. Cheap on 2028 free cash flow guidance of $8.0–8.4B.

Intel at $44: trading at roughly 1.0x its announced fab capex plan through 2030. The U.S. government bought in at $20.47. NVIDIA at $23.28.

Nokia at $13: ~4x estimated 2027 EBITDA. About half the multiple of comparable U.S. AI-infrastructure peers — despite a partner list that reads NVIDIA, T-Mobile, and the U.S. telecom system.

The Trade Behind the Trade

Here’s what GE, Intel, and Nokia all teach.

The thing you thought was the disease was actually the cure.

GE’s debt pile, which everyone called a death sentence, became the discipline mechanism that forced the breakup that unlocked $620B of value.

Intel’s manufacturing problems, which everyone called a strategic catastrophe, became the political crisis that justified the government stake that anchored the turnaround.

Nokia’s failure in phones, which everyone called a generational embarrassment, became the focusing event that left the company with exactly the assets — Bell Labs, a global telecom-equipment business, no consumer distractions — that NVIDIA needed in 2025.

In each case, the failure was not the failure.

The failure was the clearing.

It removed everything that wasn’t essential. It produced the lean, focused, undervalued entity that could ride the next wave when the next wave came.

None of the three anticipated the wave. None of them positioned for it. They just happened to be standing in the right part of the river when the current changed — having been pushed there by what looked like the worst luck imaginable.

The Lesson

The companies that get written into the history books aren’t always the ones that succeeded the most spectacularly.

Sometimes they’re the ones that survived the most quietly.

The ones who turned out, when the lights came back on, to be the only ones still in the room.

Three of those companies are walking around right now.

GE Aerospace. Intel. Nokia.

The market is starting to notice.

It’s later than it was last year. It’s earlier than it will be next.

The clearing has already happened. The wave is here.

The trade is the wait that’s already over.

Risk isn’t volatility. It’s the atrophy of learning — measured in how fast you recover.

Guillermo Valencia A.

Co-Founder, MacroWise

Medellín , Colombia